CPNG - Coupang Deep Dive

The Elephant in the Room

Coupang is effectively “Korea’s Amazon” (Just without AWS, Jeff Bezos, and the American Consumer)—a vertically integrated e‑commerce and logistics platform dominating one of the most advanced online markets in the world. At today’s valuation, the question is less whether it grows, and more how much of the total addressable market (TAM) is already priced in

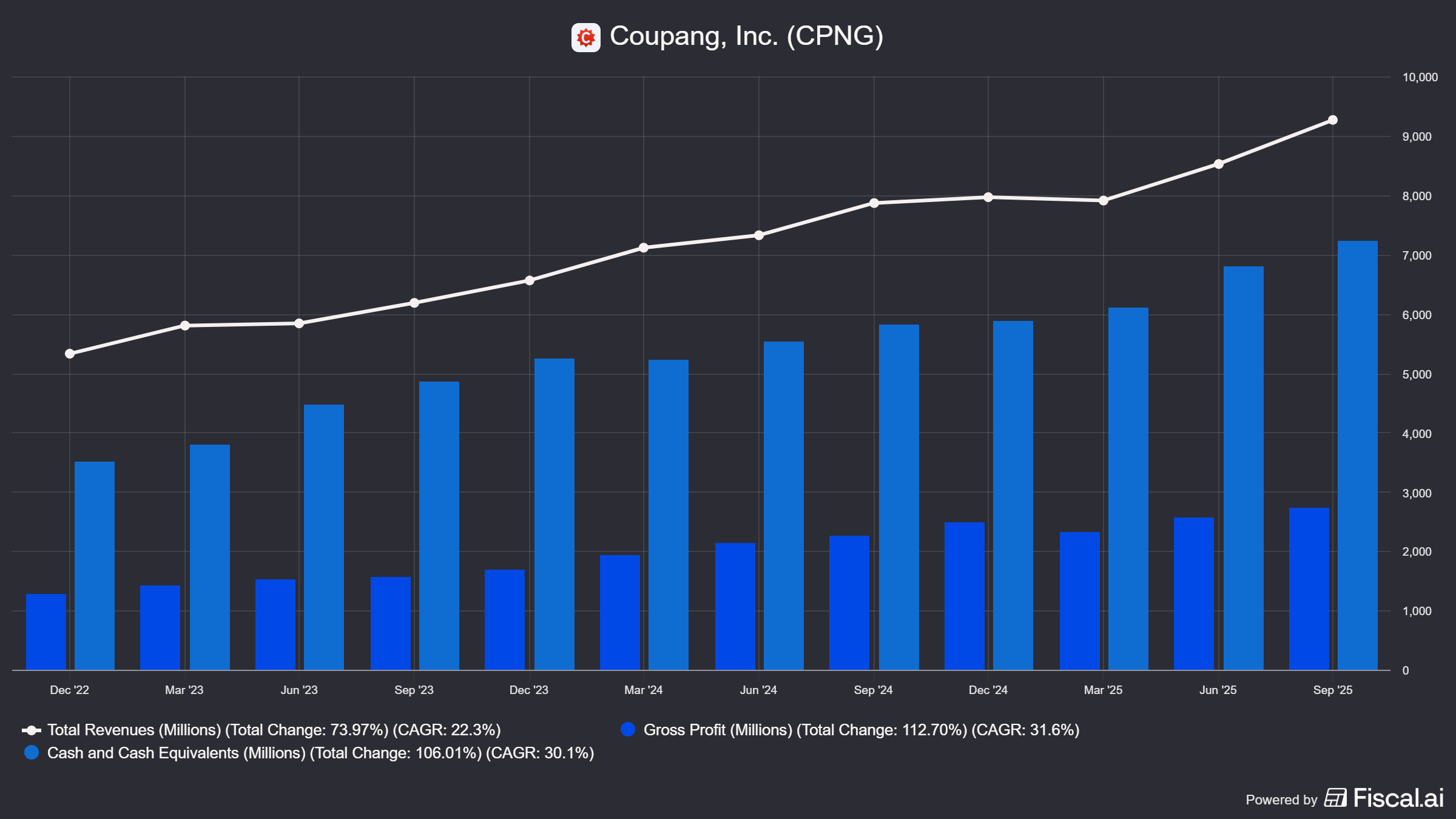

Revenue, Gross Profit, and Cash Position

The Business Itself

South Korea’s largest e‑commerce platform, combining 1P inventory, 3P marketplace, and services

Q3 2025 revenue: $9.3B, up 18% YoY (20% FX‑neutral).

Gross profit: $2.7B, +20% YoY; gross margin ~29.4% (+51 bps).

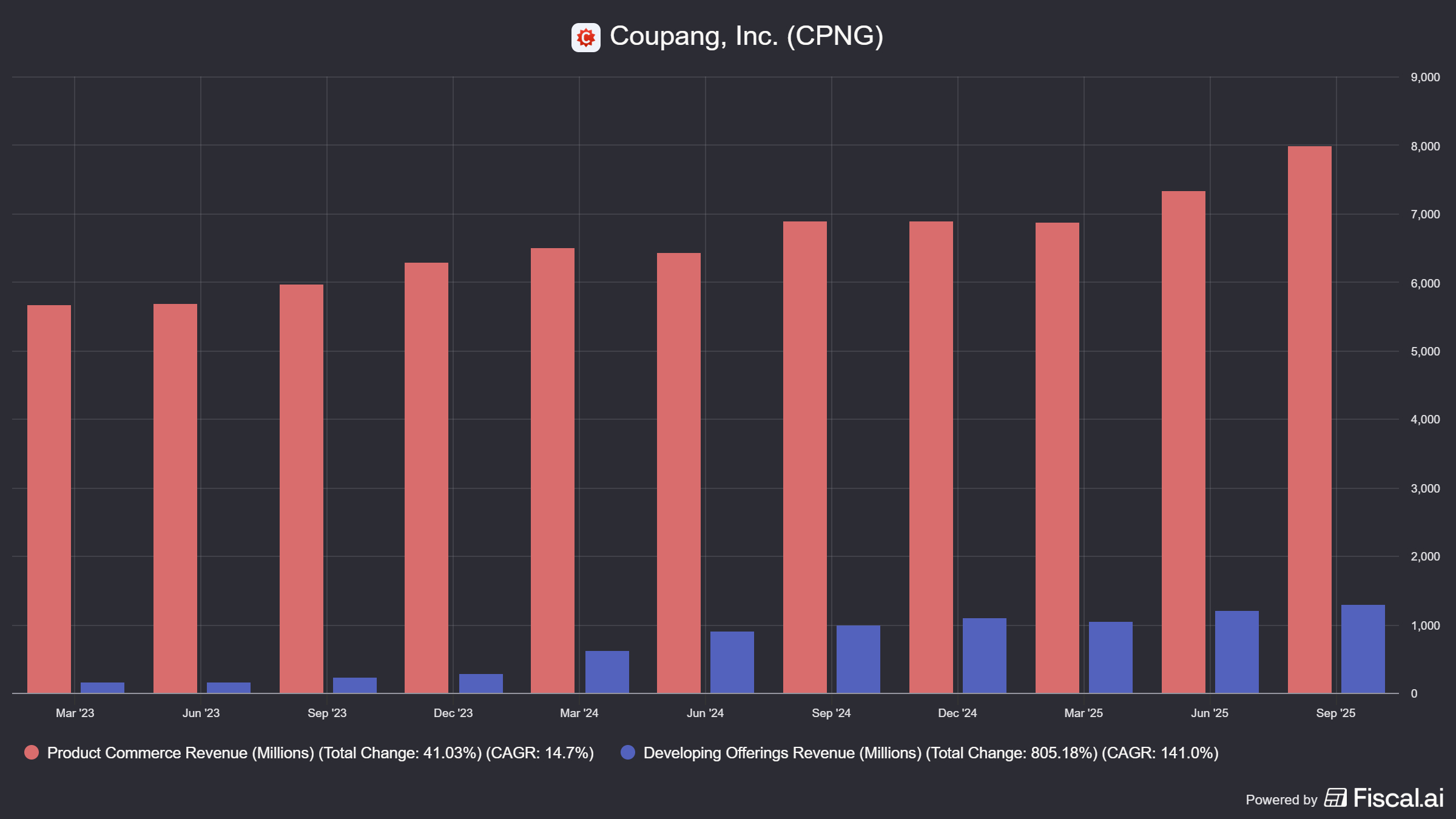

Product Commerce (core Korea):

Revenue $8.0B, +16% YoY.

Adjusted EBITDA $705M, margin 8.8% (+201 bps).

Active customers: ~24.7M, +10% YoY, in a country of ~52M people.

Coupang has reached scale and profitability in its home market while still posting mid‑teens to high‑teens top line growth.

Commerce Revenue vs Other Offerings

Valuation: TAM, Growth, and What’s Price In

South Korea E‑Commerce Context

South Korea B2C e‑commerce market: around $230B in 2024, projected to $330B+ by 2027 (~10–13% CAGR) in some studies; others see 4–5% annual growth as the market matures.

Coupang is estimated to hold roughly 35–40%+ share of online GMV in Korea, making it the clear scale player.

The structural backdrop is favorable: high urban density, fast internet, and one of the highest online shopping penetration rates globally (>80% of consumers).

Implied Multiples

At roughly 0.8–1.0x current TTM sales and around 1.0–1.2x forward 2026 sales, depending on your growth assumptions.

On profitability, TTM adj. EBITDA of $1.64B suggests an EV/EBITDA multiple in the low‑ to mid‑teens range, again modest for a scaled, growing platform.

Several DCF‑based and fair‑value estimates sit in the mid‑20s to mid‑30s per share, implying ~40–100% upside if Coupang delivers mid‑teens growth and high‑single‑digit to low‑double‑digit EBITDA margins over the next 3–5 years.

Growth vs TAM

For today’s price to make sense, you do not need heroic TAM assumptions:

If Product Commerce grows revenue ~10–12% annually as Korea’s e‑commerce market matures, and Developing Offerings compound 20–30%+ while moving toward breakeven, consolidated revenue can still grow low‑ to mid‑teens annually for several years.

If consolidated adj. EBITDA margin expands from 4.9% TTM to 8–10% over 5 years (driven by scale, automation, ads, and mix), you get a business earning $3–4B+ in EBITDA on a mid‑$40B+ revenue base.

Put simply: at roughly 1x forward sales, the market is not pricing in a dominant, 10%‑margin platform in a rich economy—it’s pricing in either (a) a structurally lower margin profile, (b) slower growth, or (c) a meaningful regulatory/brand impairment after the breach. Or, its pricing in the elephant.

The Elephant in the Room

South Korea’s population is now shrinking, with extremely low fertility and rapid aging driving long‑term decline.

Current population and growth

Total population in 2026 is about 51.6 million, down from around 51.7 million in 2024–2025.

Annual population growth has turned negative, around −0.1% to −0.13% per year recently, reflecting more deaths than births and limited net immigration.

Fertility and births

South Korea has one of the world’s lowest fertility rates; the total fertility rate was about 0.72 children per woman in 2023 and about 0.75 in 2024, far below the replacement level of 2.1.

Provisional government and media data suggest a modest rebound, with fertility around 0.79–0.8 in 2025 and roughly 0.85 in the first half of 2026, though still deeply below replacement.

Annual births are roughly in the low‑ to mid‑200,000s, and even with the recent uptick, the country continues to record natural population decline because deaths remain higher.

Aging and workforce impact

South Korea’s population has aged rapidly; median age has risen by nearly 28 years since 1950, reflecting low fertility and high life expectancy (around mid‑80s years).

The working‑age population (15–64) is projected to fall sharply, with estimates of a drop from about 37 million in 2020 to roughly 24 million by 2050, worsening pension and labor‑force pressures.

How Will This Impact the Growth Story for Coupang?

At first glance you might ask how could Coupang continue its growth trajectory if its key market is literally growing smaller by the year? That is a valid question.

Long‑run TAM cap: Over multiple decades, a structurally shrinking and aging population means fewer total consumers in its core market, even if per‑capita spend and online penetration rise.

Near‑ to medium‑term offset:

The demographic squeeze is slow, not sudden. Over the next 5–10 years, online share gains, wallet‑share expansion, and category mix (groceries, healthcare, services) can still drive mid‑teens revenue growth, even as headcount trends down.

An aging population is not uniformly bad for e‑commerce: “active seniors” have rising disposable income and are gradually adopting digital payments and online shopping, though adoption is slower than younger cohorts

Net, the birth‑rate collapse is a real ceiling on very long‑duration TAM. It doesn’t kill the 3–7 year Coupang thesis, but it does argue against modeling Korea as a forever 10–15% growth engine. The good news, I think the company is being discounted already for this terminal growth for the core market. AKA, its priced in. Therefore, any uptick or shift to population growth, or Coupang adoption in other geographies that are growing, that then creates real upside for the share price.

Technicals

The recent data breach news has sent the stock price well below its 200D but might be setting up an oversold bounce soon (at a minimum)

Looking at the weekly, I have placed key levels to look for resistance and support, with the current RSI read on the weekly I can definitely see a bounce to that 19 level to start, and any upside catalyst around regulators (unknowns becoming knowns) can push it quickly to the 2nd target near 22.

Dark Pools

There have been several large prints to start 2026 so not much of an edge, but there was a nice #29 rank that hit last week.

Final Thoughts

I have a positive bias for Coupang, I like the Founder and CEO, think the right leaders can be what separates great companies, but the risk is real with the Korean government laying heavy penalties for the data leak, the population decline in their key geography, and an already large market share of the Korean market. What makes Amazon the monster that it is, is that it isn’t afraid to try new things, such as AWS. These are calculated risk that pay out with the right leadership, maybe Coupang has that. If you think they do, this could be an incredible long term opportunity. The valuation argument is there and the technicals are ugly but do encourage seller exhaustion may be near. My own thesis here, I like it for a trade. I’m willing to take CPNG on a date, but I’m not putting a ring on it. Not yet anyway.

Trade Idea, long shares near 17 with 1st target at 19.07, a 10% profit. 2nd upside target near 22 can net >30% gain. Final Target at 25.30’s, 47% gain.

Hope you all enjoyed the content, if you have any other companies you want a report on just reach out. Each week there are new trade idea’s, market analysis, and live updates throughout the date with our paid subscribers. Just reach out if you want a trial run. Cheers!

Well done! Would be great to see the political overhang come off this name and reprice on fundamentals.