Kymera Therapeutics

The Oral Biologic Bet the Best Biotech Funds Are Quietly Stacking

The Setup

Every quarter, biotech-only hedge funds — the ones that live and die by clinical readouts — quietly tell you what they think will work over the next 24 months. You just have to read 13Fs and resist the temptation to chase whatever oncology name is trending on FinTwit.

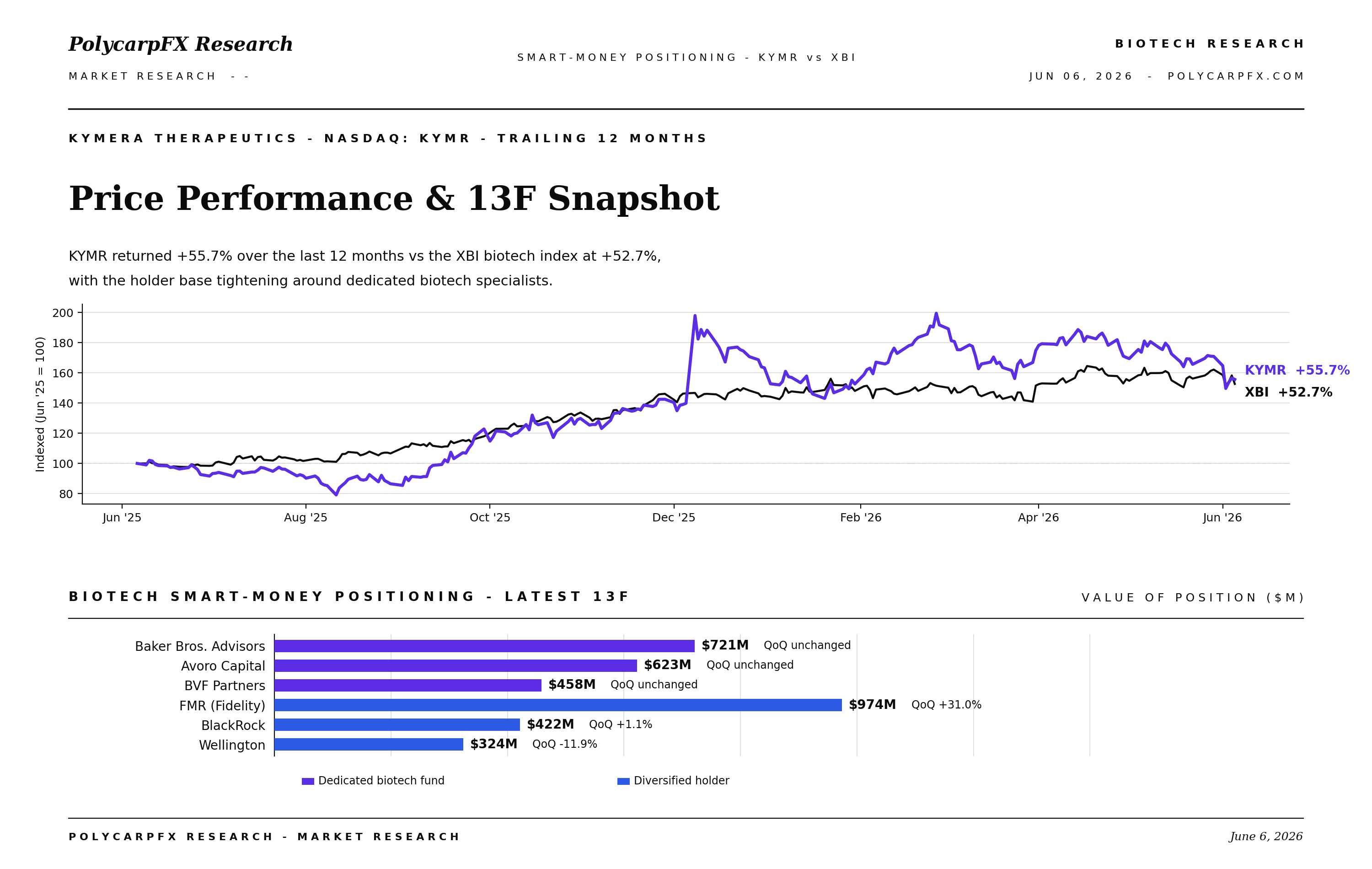

This week, the signal is loud and the name is underrated outside the specialist community: Kymera Therapeutics (NASDAQ: KYMR). According to Stifel’s May 2026 Biotech Buyside Study, KYMR is the #1 biopharma holding at BVF Partners — one of the most disciplined dedicated biotech funds in the country. Baker Bros, Avoro, and BVF together own more than 21M shares — over $1.8B of position value at current prices, and that’s before we count generalists like Fidelity stacking another $974M.

Risk signal worth flagging: Perceptive Advisors shows -100% QoQ — they fully exited. Perceptive runs a more event-driven book than Baker/Avoro/BVF, so this is best read as profit-taking rather than a thesis change

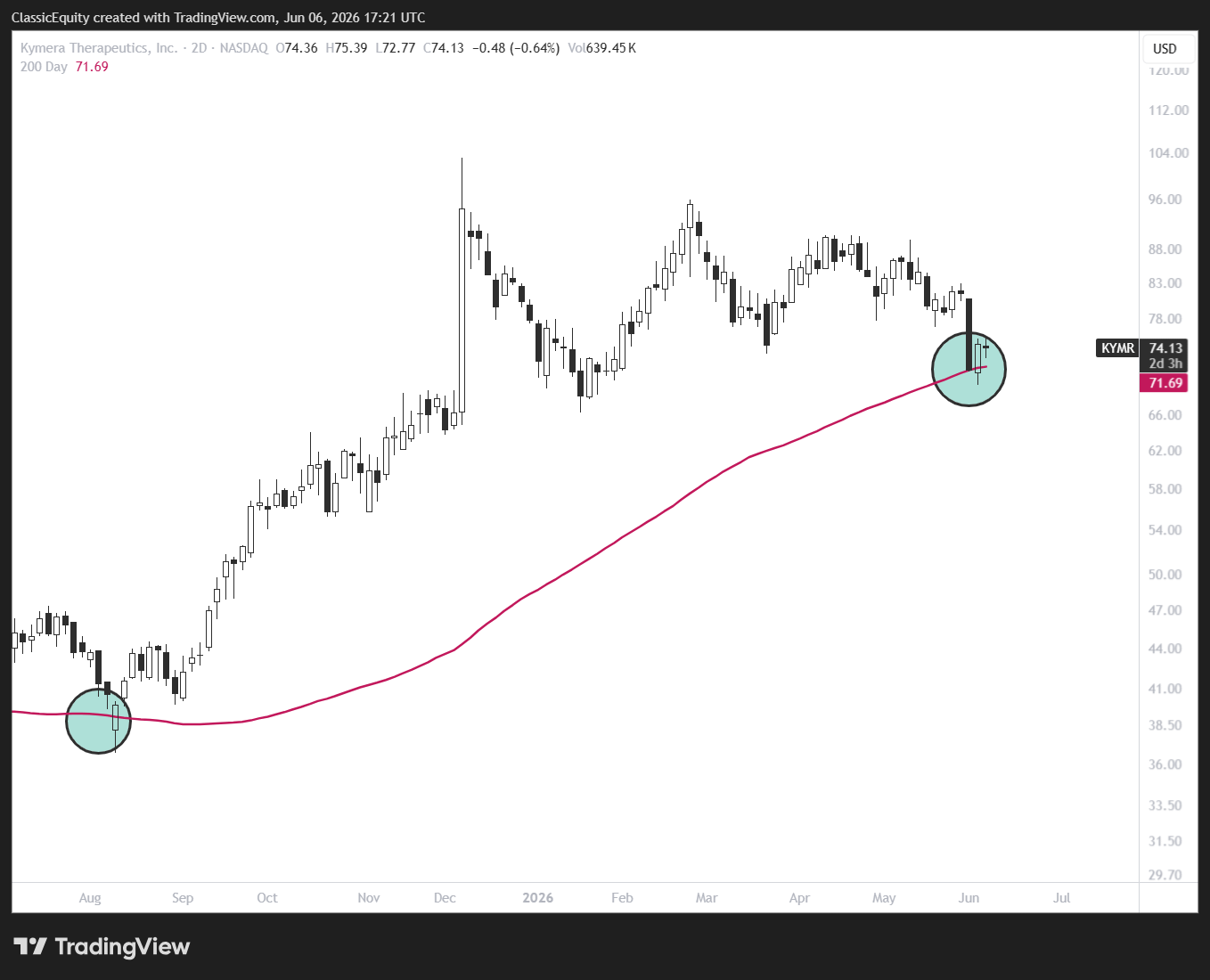

Shares closed $74.13 on Friday and recently bounced off the 200D (near 71.69), putting the market cap at $6.10B. The 52-week range is $36.65 to $103, so the stock is still ~28% below its highs despite a string of positive clinical reads. Wall Street’s 18 covering analysts are 100% bullish with an average price target of $120.72 — implying 62.8% upside — and the spread runs from $100 low to $140 high.

What Kymera actually does

Kymera is the leading independent pure-play in targeted protein degradation — small molecules that bind a disease-driving protein and physically destroy it via the body’s own ubiquitin-proteasome system. Think of it as a heat-seeking missile that removes pathologic proteins instead of just inhibiting them.

The headline asset is KT-621, an oral degrader of STAT6 — the master transcription factor downstream of IL-4 and IL-13 signaling. Translation: if it works, it does what Dupixent (Dupilumab) does — Sanofi/Regeneron’s $13B+ blockbuster injectable for atopic dermatitis and asthma — but as a daily pill.

The Phase 1b BroADen readout in December 2025 delivered the kind of data biotech bulls dream about:

• 98% blood STAT6 degradation, 94% skin degradation, 74% TARC reduction in 22 moderate-to-severe atopic dermatitis patients

• Clean safety, well tolerated

• FDA Fast Track designation already in hand for AD

Two pivotal Phase 2b trials are now enrolling:

• BROADEN2 (Phase 2b atopic dermatitis): dosing initiated Nov 2025, topline mid-2027

• BREADTH (Phase 2b eosinophilic asthma): dosing initiated 2026, topline late-2027

The investment question is no longer “does STAT6 degradation translate to clinical efficacy” — Phase 1b answered that. The question is “can it match a biologic in a placebo-controlled Phase 2b on real efficacy endpoints?”

If yes, the Total Addressable Market is the entire IL-4/IL-13 biologic franchise — and an oral pill at a fraction of the price destroys the injectable’s moat overnight.

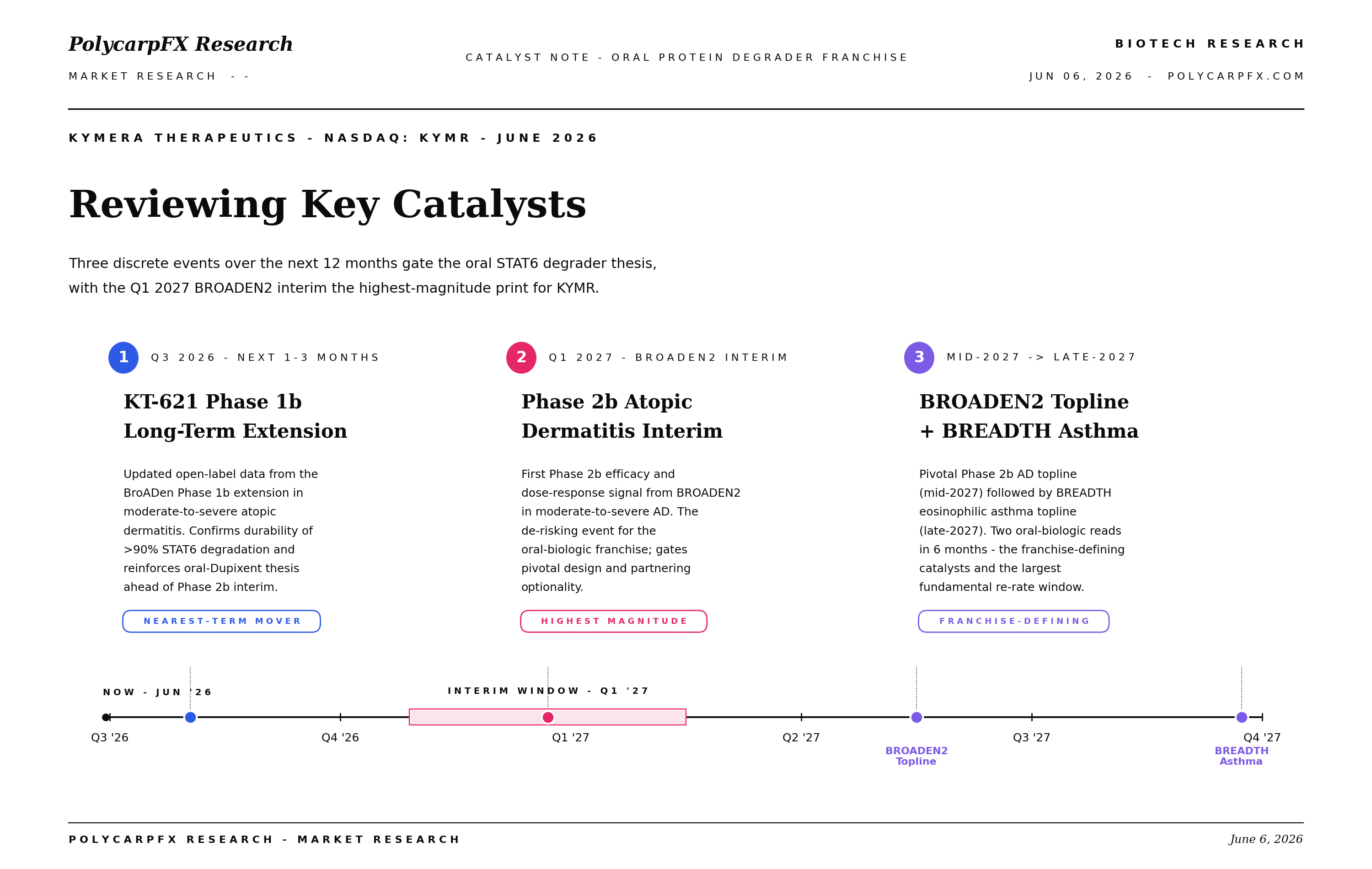

The next 12 months — three catalysts that move the stock

1. Q3 2026 · KT-621 long-term extension data (NEAREST-TERM MOVER). A continuation of the Phase 1b BroADen open-label extension. The bar is durability — confirming that >90% STAT6 degradation holds with chronic dosing and that the clean safety profile carries. Not a re-rate event by itself, but a confidence builder ahead of #2.

2. Q1 2027 · BROADEN2 interim (HIGHEST MAGNITUDE). First Phase 2b efficacy and dose-response signal in moderate-to-severe AD. This is the de-risking event for the entire oral-biologic franchise. A clean interim gates pivotal design, partnering optionality, and likely triggers a step-change in consensus PT distribution. The current $100–$140 PT range will collapse upward or downward off this print.

3. Mid-2027 → Late-2027 · BROADEN2 topline + BREADTH asthma topline (FRANCHISE-DEFINING). Two oral-biologic Phase 2b reads in six months. This is the largest fundamental re-rate window of the decade for KYMR. Successful reads turn KT-621 into a partner-able / pre-commercial asset; failed reads reset the equity story to the rest of the degrader pipeline (which is real, but not what the multiple is built on).

Financials — does the balance sheet survive to the catalyst?

• Revenue: $34.4M (Sanofi collaboration milestones + research funding)

• R&D: $98.2M

• Operating loss: -$84.2M

• Net loss: -$69.2M

• Cash: $144.1M

• Short-term investments: $506.8M

• Total liquidity: $651M

• Operating cash burn (Q1): -$88.8M → annualized burn $355M

• Cash runway: 1.8 years (conservative — assumes zero new collaboration revenue and ignores any milestone earn-outs from Sanofi)

Read carefully: 1.8 years of runway from March 31, 2026 puts the cash-out date squarely past BROADEN2 interim (Q1 2027) and right up against BROADEN2 topline (mid-2027). Management has multiple financing optionality windows — a positive Q1 ‘27 interim is almost certainly the trigger for an opportunistic raise at a much higher price.

This is a healthy balance sheet for a Phase 2b biotech with a pipeline that has already de-risked Phase 1.

Valuation framing

At $6.1B market cap and ~$651M cash, enterprise value is roughly $5.5B. For comparison, the IL-4/IL-13 franchise (Dupixent) does well over $13B in annual sales today. If KT-621 captures even a low single-digit share of that franchise as an oral alternative — and that’s before you assign credit to the rest of Kymera’s degrader pipeline — the current EV looks rational, not stretched.

The 18-analyst average target of $120.72 (high $140, low $100) implies the Street is already pricing in a partial probability of Phase 2b success. The upside case re-rates further on interim data; the downside case is gated by balance sheet, not by an immediate cash crunch.

How I’m thinking about it

The setup I want for a binary biotech is:

Asset with mechanistic validation already on the board — Phase 1b STAT6 degradation: checked

Multiple shots on goal at the same target — BROADEN2 + BREADTH = two Phase 2b reads, six months apart

Dedicated biotech HFs holding firm at near-peak position sizes — Baker, Avoro, BVF all unchanged at multi-hundred-million-dollar positions

Balance sheet survives to the catalyst with optionality to raise from strength — 1.8 years runway, $651M

Realistic upside-to-downside skew — 62.8% to consensus PT, with high end implying ~89% upside

Watch item: Perceptive’s full exit. Worth tracking next 13F to see if Baker/Avoro/BVF stay put.

That’s a clean setup. Not without risk — biotech Phase 2b interims have a 30–40% failure rate historically — but it’s the kind of setup specialist money is built to underwrite.

KYMR sits with a defined plan: scale risk into the Q3 2026 long-term extension data, with the real position size decision gated by the Q1 2027 BROADEN2 interim print

Hope you enjoyed the read, if you aren’t a paid subscriber, consider joining the team as I give out company deep dives, overall market analysis, and take request all day for data and insights on your favorite companies, cheers!

Weekly Signal Report - 6/2/2026

SIGNAL OF THE WEEK - Oracle has a 100% hit rate the past ten years from June to July