Micron Technologies, AI Darling or Priced to Perfection?

Earnings This Week: Dark pool signals: recent activity worth watching

Micron Technologies reports earnings Wednesday after the close, and it’s shaping up as one of the more polarizing setups heading into the last full trading week before the holidays. The stock has been riding the AI infrastructure wave hard, but recent dark pool activity and December seasonality suggest this print could be messier than the bulls expect.

The fundamental case: strong, but priced for perfection

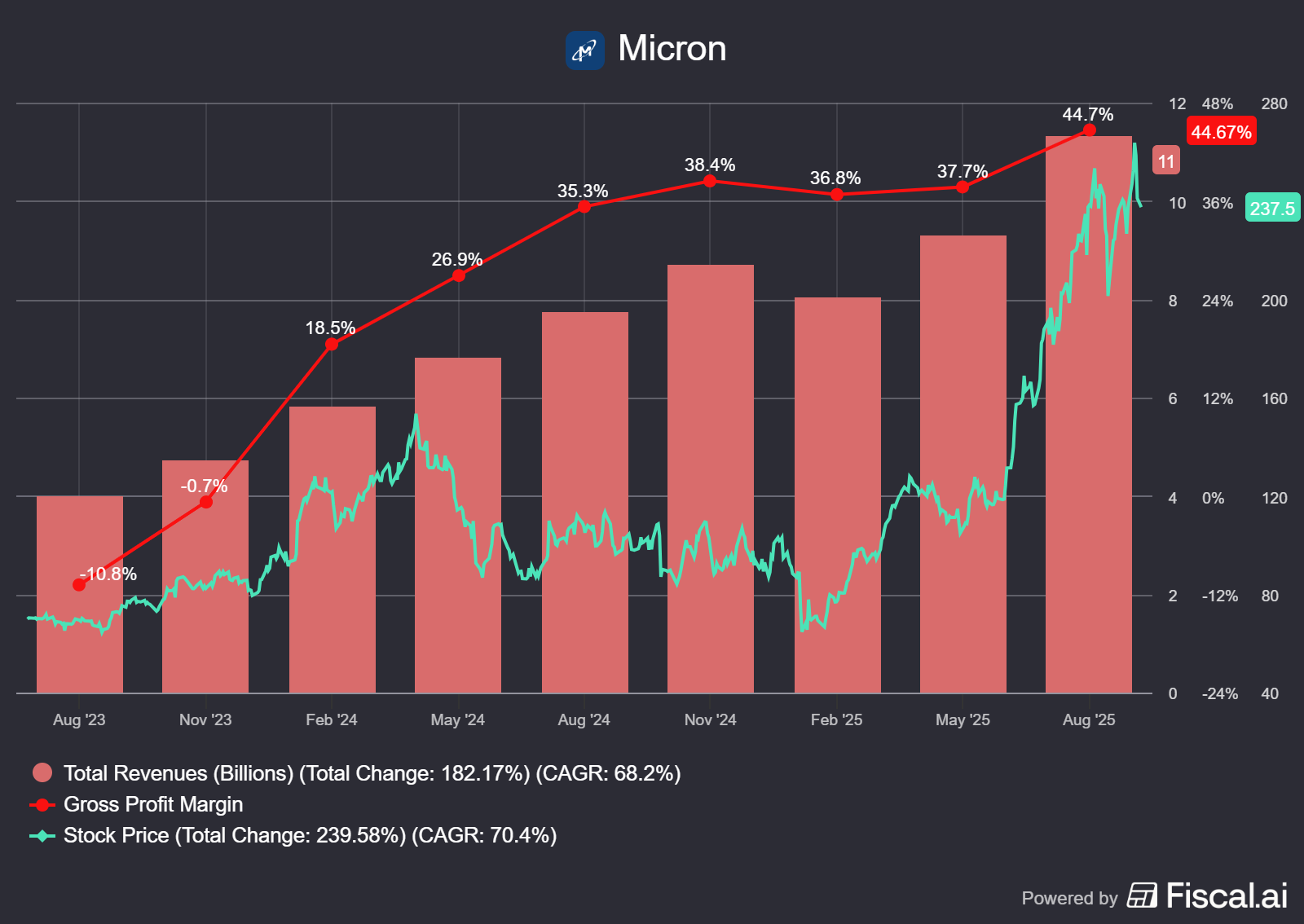

Micron is a beneficiary of the multi-year memory upgrade cycle driven by AI data centers, high-bandwidth memory (HBM), and enterprise demand for DRAM and NAND. The company has transformed from a cyclical commodity play into a structural growth story, with analysts projecting revenue growth in the mid-teens for fiscal 2025 and 2026 as hyperscalers (Microsoft, Amazon, Google) build out AI compute infrastructure that requires increasingly sophisticated memory architectures.

HBM is the crown jewel here. Micron’s HBM3E product is now shipping to Nvidia and other AI chip makers, and management has guided that HBM revenue will exceed $8 billion in fiscal 2025—a massive jump from essentially zero two years ago. Gross margins have expanded meaningfully as the mix shifts away from commodity PC/mobile DRAM toward these higher-margin, AI-specific products. Operating leverage is strong, and free cash flow generation is back after years of cyclical trough conditions.

That said, the stock is no longer cheap. Micron trades at a premium to its historical range on both P/E and EV/sales, reflecting the market’s belief that this cycle is different and that AI memory demand insulates the company from the brutal boom-bust patterns that historically plagued the sector. The question is whether the current valuation already discounts several quarters of flawless execution and whether any guidance miss or caution around calendar 2026 orders triggers a violent de-rating.

AI narrative: real, but crowded

Micron’s AI exposure is legitimate. HBM is essential for training and inference in large language models, and Micron is one of only three suppliers globally (alongside Samsung and SK Hynix) with the technology to produce these chips at scale. The company is sold out through 2025, and early 2026 capacity is largely committed.

The risk is that the AI narrative is now consensus, fully priced in, and vulnerable to any sign of a pause in hyperscaler capex. We’ve already seen some caution from cloud providers around spending efficiency, and if Micron’s guidance suggests Q2 or Q3 fiscal 2026 (calendar Q1/Q2 2026) could see softer sequential growth, the market may interpret that as the start of a digestion period. Memory is still cyclical, even if the cycle is now driven by AI rather than smartphones, and any hint that supply is catching up to demand faster than expected will weigh on multiples.

Underrated risk: traditional end markets are still weak

While AI memory is booming, Micron’s traditional end markets—PC, mobile, and consumer electronics—remain soft. DRAM and NAND pricing in these segments has stabilized but not recovered to prior cycle peaks, and there’s limited visibility on when a true replacement cycle might kick in for PCs or smartphones. If AI revenue growth decelerates even modestly while legacy businesses stay flat, the overall growth story breaks down, and the stock’s premium valuation becomes difficult to justify.

Additionally, China exposure remains a wildcard. Micron generates a significant portion of revenue from Chinese customers, and any escalation in U.S.–China tech restrictions or retaliatory actions by Beijing could disrupt shipments or force margin-dilutive rerouting of supply chains.