Money for Rockets: The SpaceX IPO Deep Dive

Here’s how to trade the largest listing in history without becoming the exit liquidity

The thesis in one sentence: SPCX is a low-float, mechanically-bid, retail IPO sitting on a ~94× sales valuation and a staggered insider supply schedule — built to squeeze first and bleed later, so the entire edge is knowing which of four windows you’re trading.

What’s actually printing

Strip the Mars poetry and here’s the deal that prices after the close on June 11 and trades June 12 on Nasdaq as SPCX:

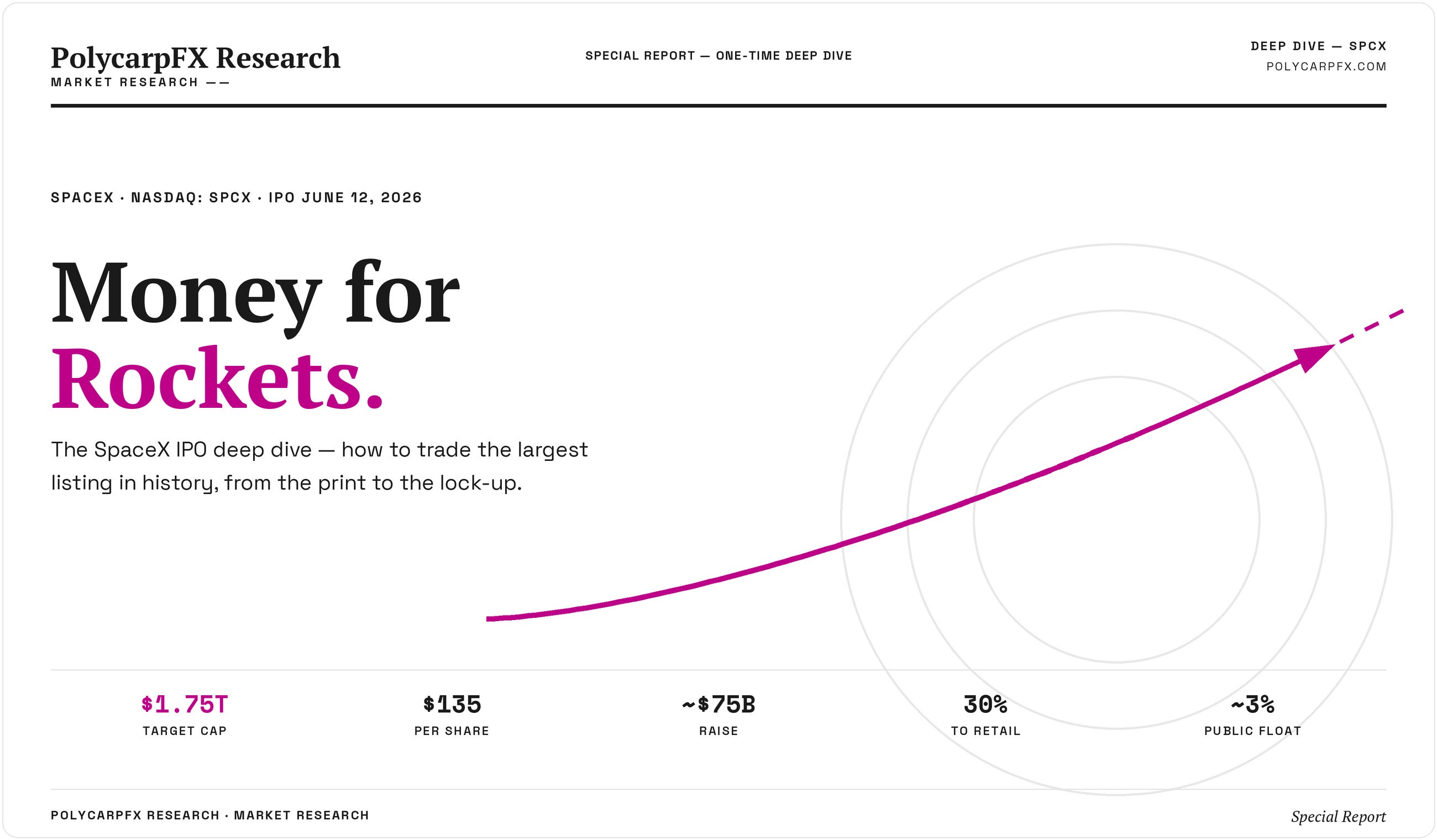

$135/share, fixed. No range, no bookbuild dance — they handed the market a number and walked. ~556M shares, ~$75B raised, ~$1.75T target cap. Largest IPO ever, ~2.5× Aramco.

30% reserved for retail. Three-plus times the normal mega-cap allocation. That’s not generosity; that’s the tell. A serious institution doesn’t need to sell 30% to the crowd unless the crowd is the buyer the math requires.

~3% public float. A ~$1.75T company with a tradable base of roughly $45–100B. Remember that number — it’s the whole game.

The fundamentals they’d rather you skip: Q1’26 net loss $4.28B, accumulated deficit $41.3B, AI burning ~$2.5B a quarter. Only the connectivity (Starlink) segment makes money. Space launch revenue actually fell year-on-year.

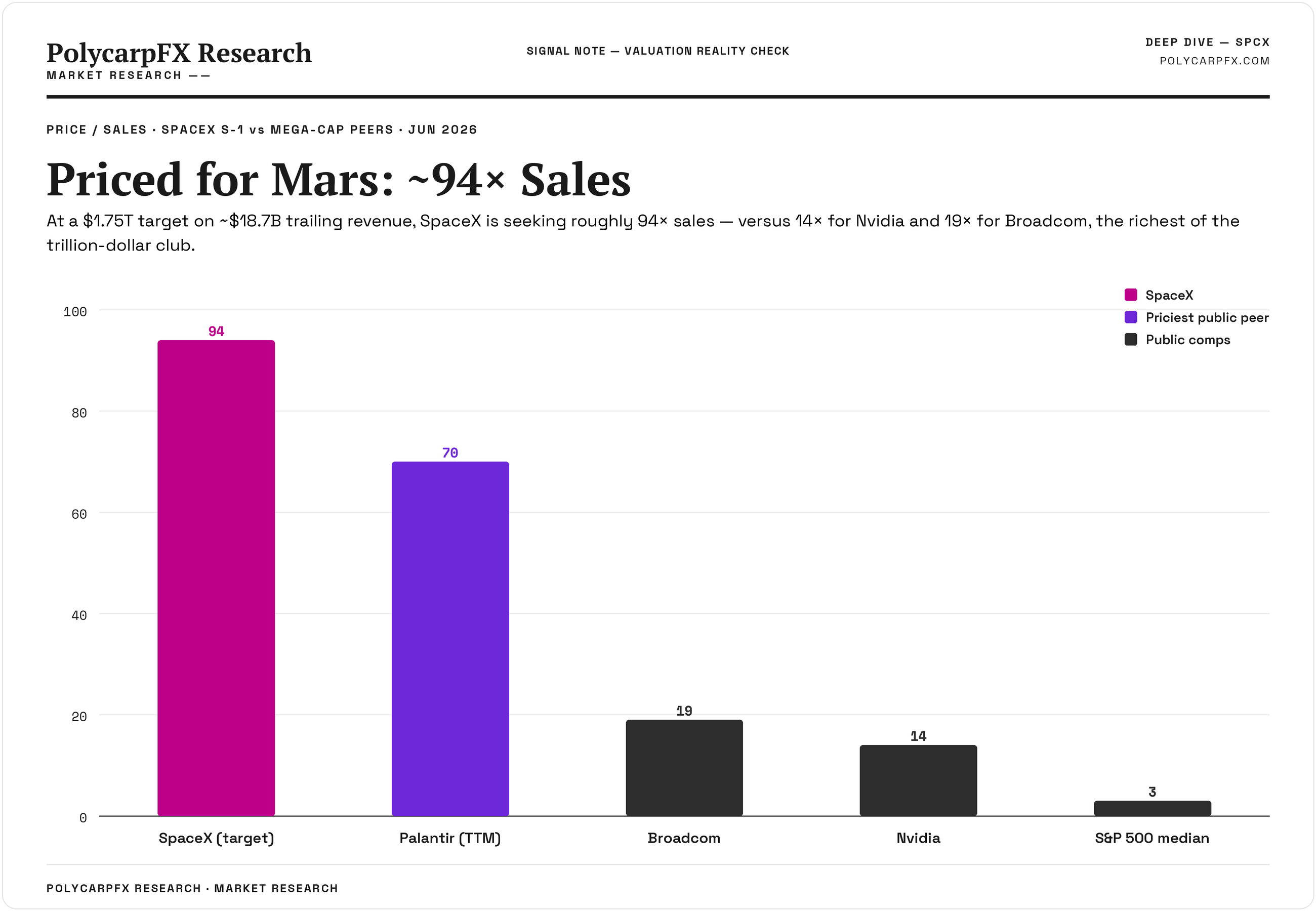

Valuation: Priced for Mars

At $1.75T on ~$18.7B trailing revenue, SPCX is asking for ~94× sales. The richest name in the entire trillion-dollar club, Broadcom, trades at ~19×. Nvidia — growing 85% — trades at ~14×. The only public comp in the same zip code is Palantir near ~70×, and Palantir is GAAP-profitable.

You don’t get to ~94× on a 9–15% organic grower with a $4B quarterly loss through DCF. You get there through a story — multiplanetary TAM, asteroid mining, data centers in orbit — and a buyer who isn’t pricing the next four quarters. That buyer is retail and, mechanically, your QQQ.

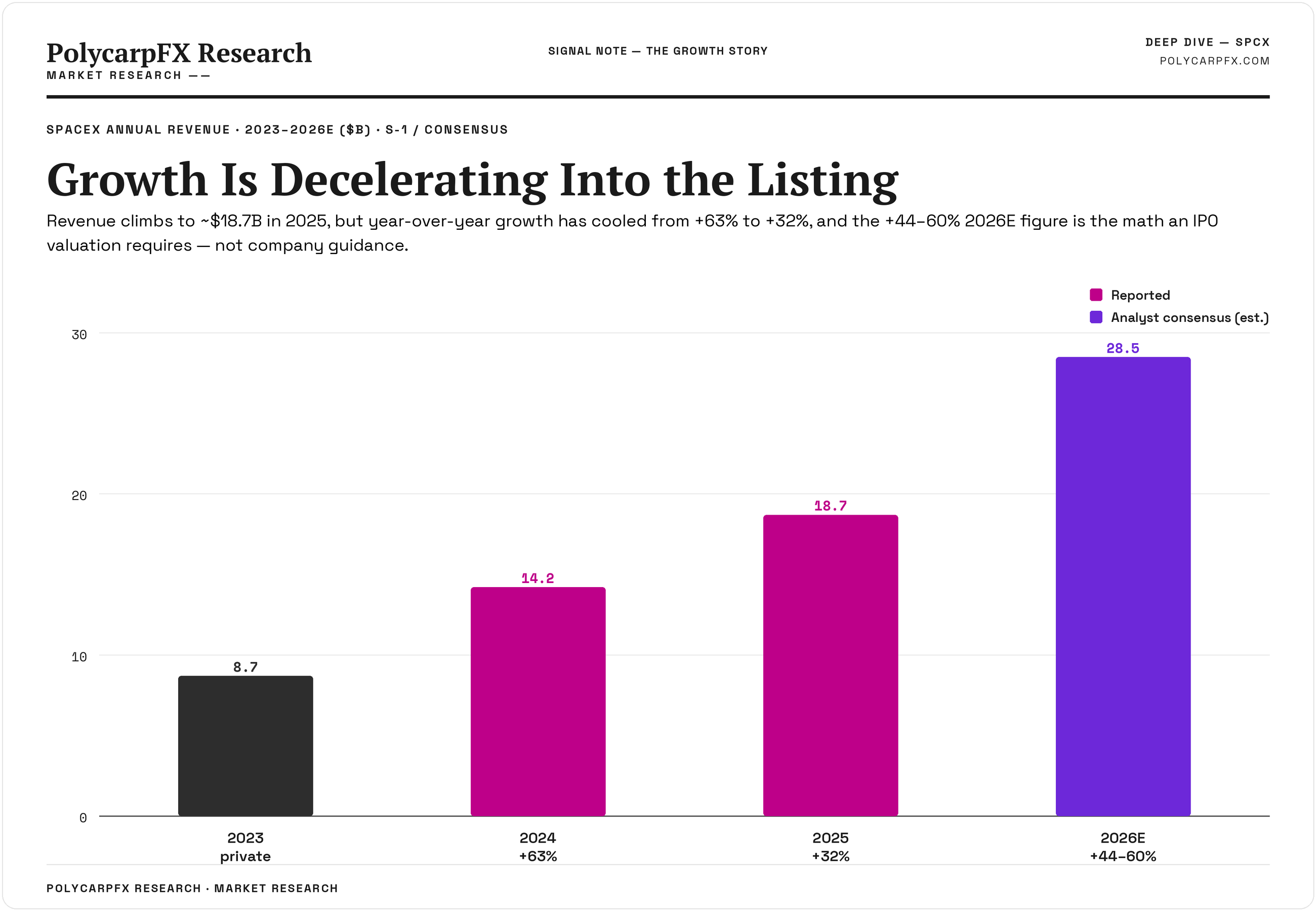

The growth is decelerating into the listing

This is the part the S-1 glosses: revenue growth has gone from +63% → +32%, and the headline +44–60% for 2026E is reverse-engineered from the valuation, not guided by the company. Strip the xAI consolidation and the core grew single digits. You’re paying a 6× revenue acceleration premium for a deceleration.

The Engine: Forced buying meets a garden hose

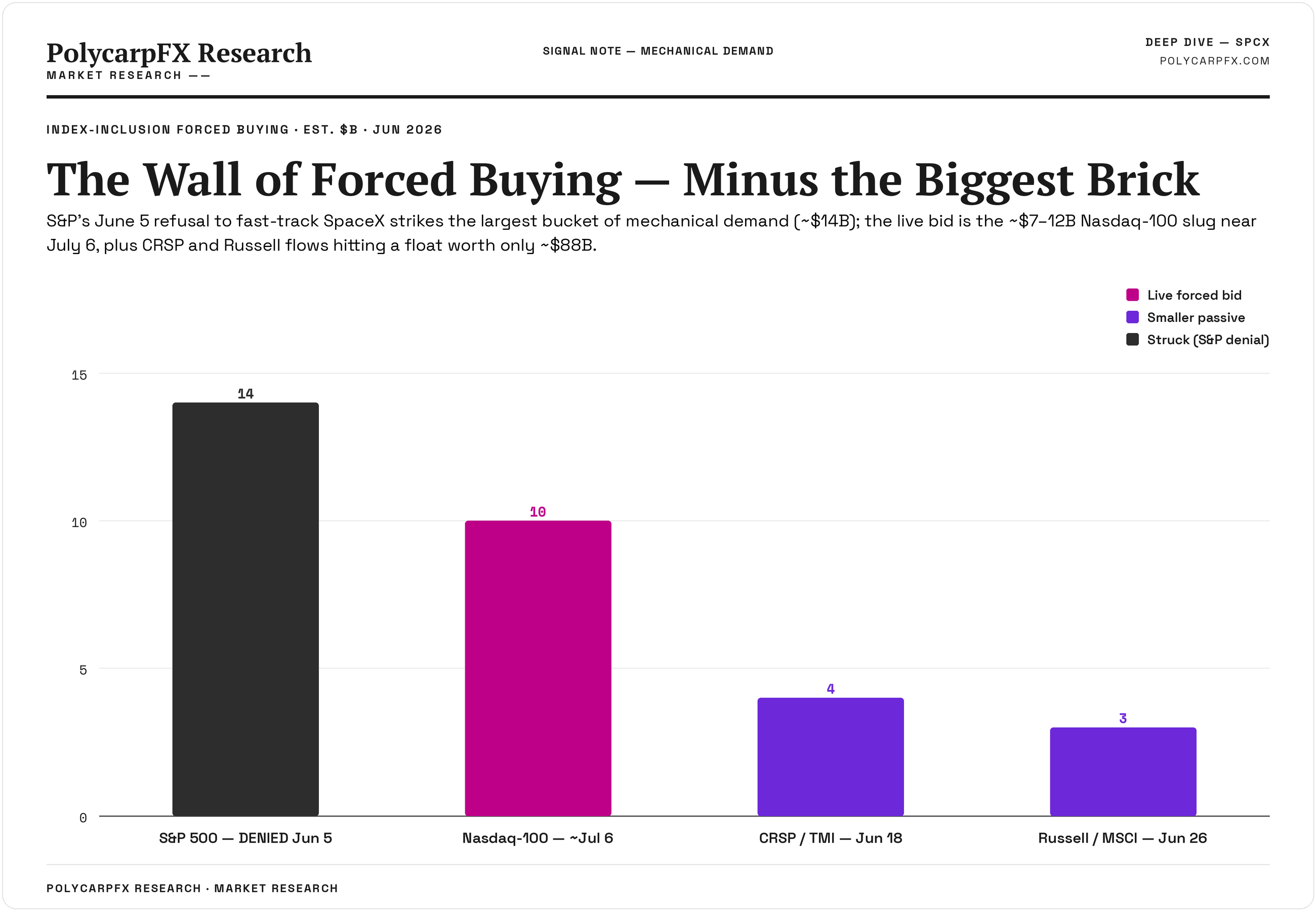

Here’s why this isn’t a normal expensive IPO. Index providers rewrote the rules to jam SPCX into benchmarks at a phantom weight, forcing passive funds to buy a stock with almost no float.

The big June 5 change: S&P Dow Jones refused to fast-track it — reaffirming 12-month seasoning, profitability, and float requirements. That single decision struck ~$14B of forced buying that the bulls were counting on. No S&P 500 inclusion until at least a year out, and only if it’s profitable. That December “SPX inclusion” everyone penciled in? Off the calendar.

What’s still live: Nasdaq’s “Fast Entry” rule survives — NDX in ~15 trading days (~July 6), free-float minimum eliminated, and a float multiplier up to 3–5× that weights SPCX as if it were a ~$400B+ free-float stock. Conservative estimate: ~$7–12B of single-day NDX-tracker buying, plus CRSP/TMI (~Jun 18) and Russell/MSCI (~Jun 26). As one widely-shared note put it, you’re forcing a firehose of mega-cap capital through a garden hose of actual liquidity.

That’s the asymmetry nobody frames correctly: low float + mechanical demand cuts both ways. Near-term it’s a squeeze risk up. The supply problem is real — but it shows up later, on the lock-up calendar, not on day one.

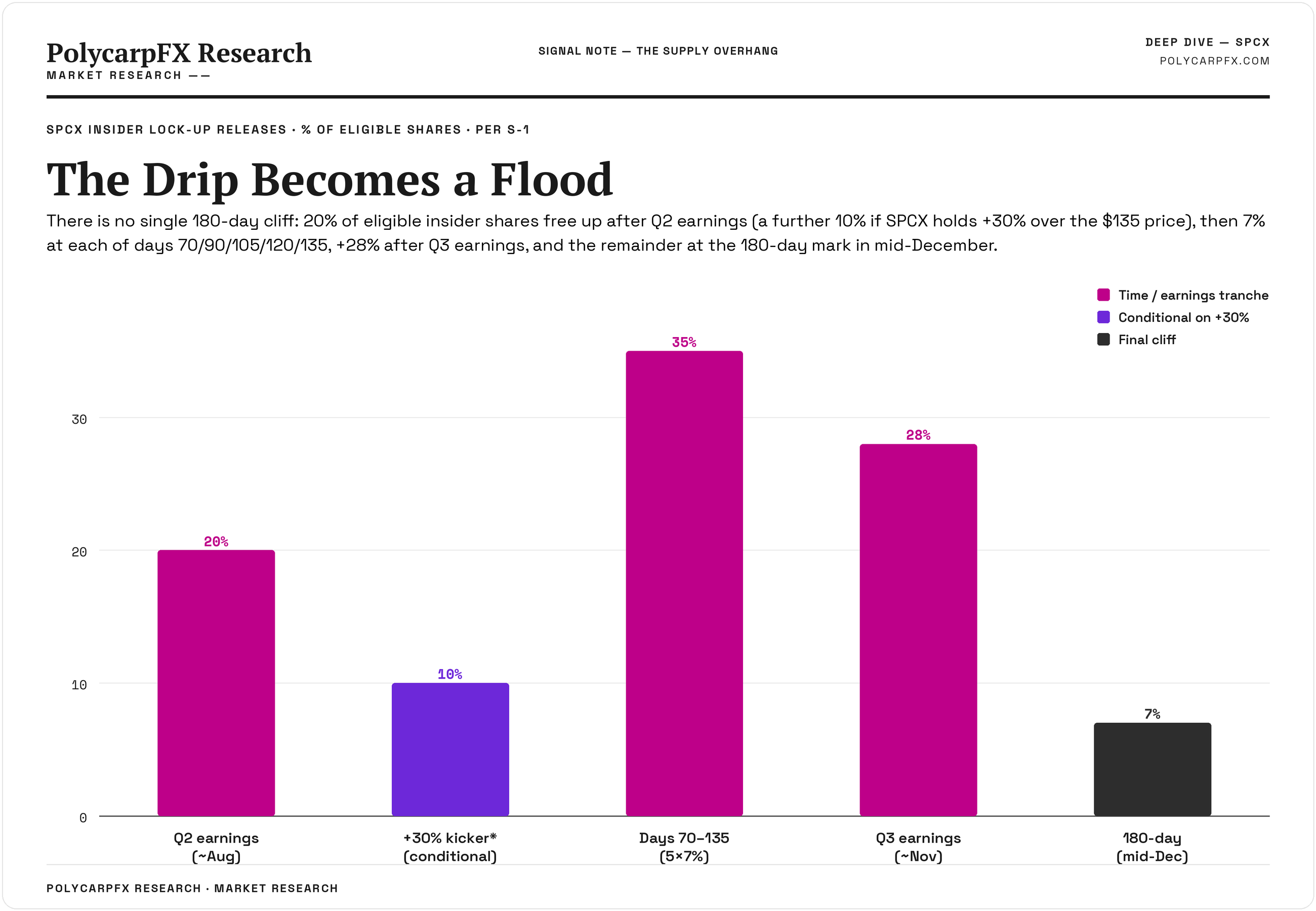

The Supply Clock: The Drip becomes a Flood

Forget the clean 180-day cliff. SpaceX built a rolling unlock that lets insiders use the crowd as exit liquidity in tranches:

~20% of eligible insider shares after Q2 earnings (~August) — +10% more if SPCX holds +30% over $135 (≈$175.50) for 5 of 10 days first. Read that twice: a strong squeeze triggers more supply. It’s self-limiting by design.

7% each at days 70 / 90 / 105 / 120 / 135 — a steady September–October drip.

+28% after Q3 earnings (~November).

Remainder at 180 days (mid-December). Musk himself: locked 366 days, no early release.

So the tape’s character flips around late August: the forced bid is spent, and the supply faucet opens and never fully closes into year-end.

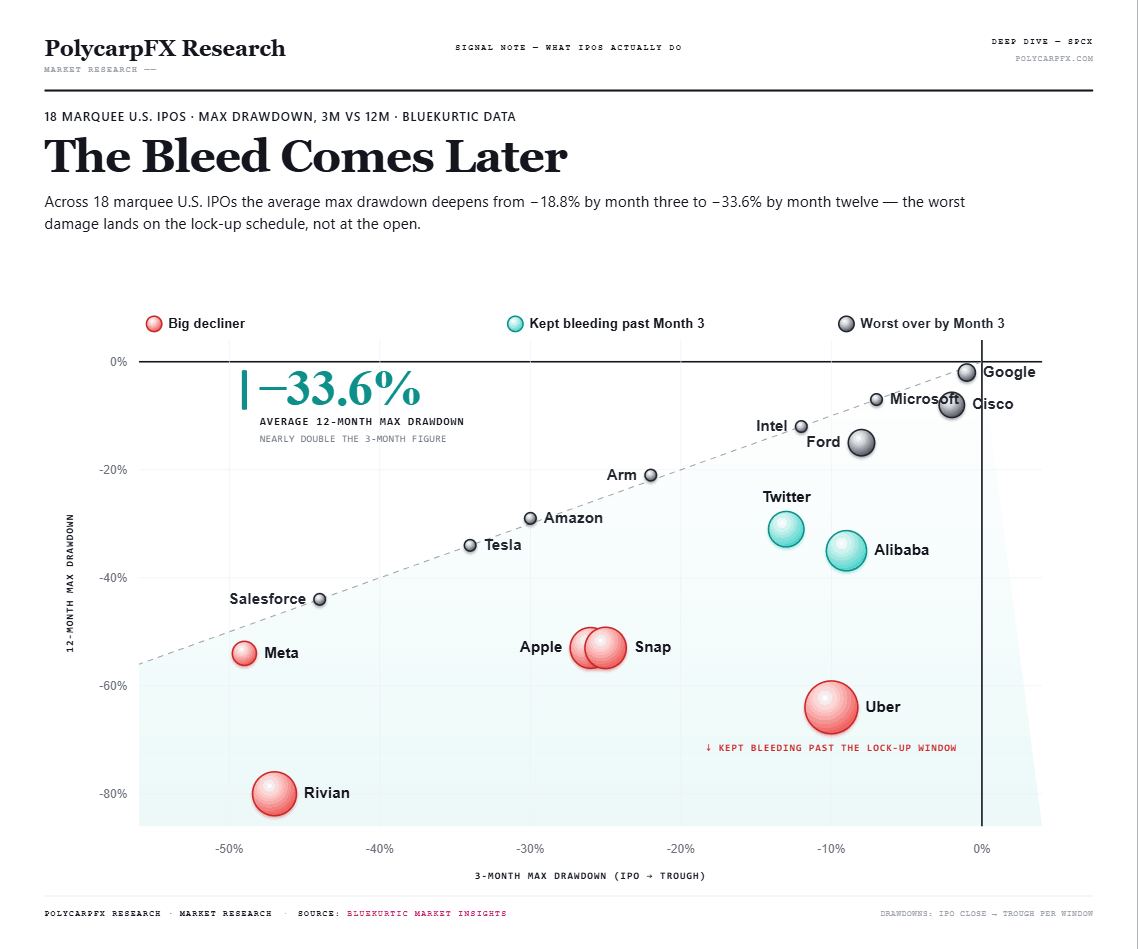

What IPOs Actually Do

Pull the tape on 18 of the most important IPOs in modern market history — Ford to Arm — and the pattern is uncomfortable for anyone planning to buy SPCX at the open. The average name lost −33.6% from its IPO price to its 12-month trough; the median, −33.0%. A roughly one-third drawdown isn’t the tail outcome here. It’s the base case.

And being right on the company didn’t save you. Apple fell −50% in its first year. Amazon −29%. Meta −54%. Tesla −34%. Every one of them became a trillion-dollar story — and every one handed early buyers a brutal year first. The names that didn’t draw down meaningfully are few and regime-specific (Google −0.4%, Microsoft −7%); the ones that got cut in half or worse — Rivian −79%, Uber −64%, Meta −54%, Snap −52% — read like a roll call of exactly what SPCX is: richly valued, heavily hyped, and carrying a wall of locked stock waiting to hit the tape.

The typical mega-IPO is down ~3% in week one and underwater at a year. The average is a lie told by a handful of Amazons, Googles, and Ciscos.

The timing is the part that matters most for this trade. The average 3-month max loss is just −18.8% — but the 12-month figure is nearly double at −33.6%. The damage doesn’t land at the open. It compounds over the following two to three quarters, which is precisely when staggered lock-ups expire and insider supply floods the market. That’s not coincidence; it’s the mechanism. For SPCX, the mechanism is already on the calendar: five rolling unlock tranches and a full 180-day cliff that collides with December’s index reconstitution.

None of this says SpaceX is a bad company. It says the IPO trade and the company are two different things. History says the first year is a drawdown machine, the worst of it arrives on the lock-up schedule, and the right side of this is positioning for the supply — not chasing the listing.

If you aren’t a paid subscriber, consider joining the team as I give out company deep dives, discord access to my own trading journal, overall market analysis, and take request for data and insights on your favorite companies, cheers!

How to Trade It: Four Windows, Four Games

Keep reading with a 7-day free trial

Subscribe to PolycarpFX to keep reading this post and get 7 days of free access to the full post archives.