Summer Vibes and Speculation

The Week Ahead 6/1/26

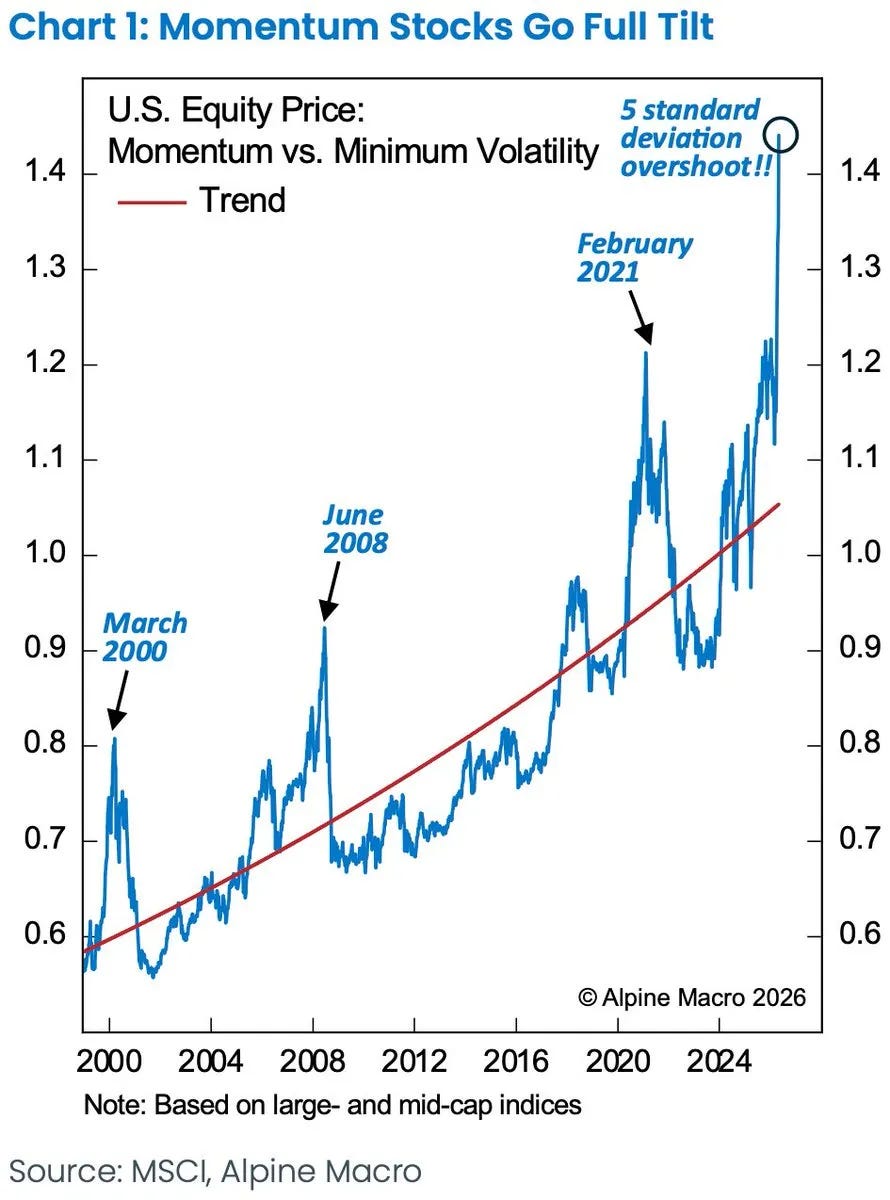

The signs of market extremes keep accumulating as a generational speculative run takes hold.

Risks and vulnerabilities are clearly building — but for now, the trend remains your friend. The speculative cycle runs until it doesn’t. May was another month where it did.

We are now entering June where we just saw the S&P continue its rally in May gaining over 5% with a sense of euphoria across the market. Some key thoughts going into next week

Stretched valuations and positioning keeps me cautious with some historical readings hitting in key sectors

June is filled with catalyst that could create some volatility but it likely remains subdued overall until August timeframe

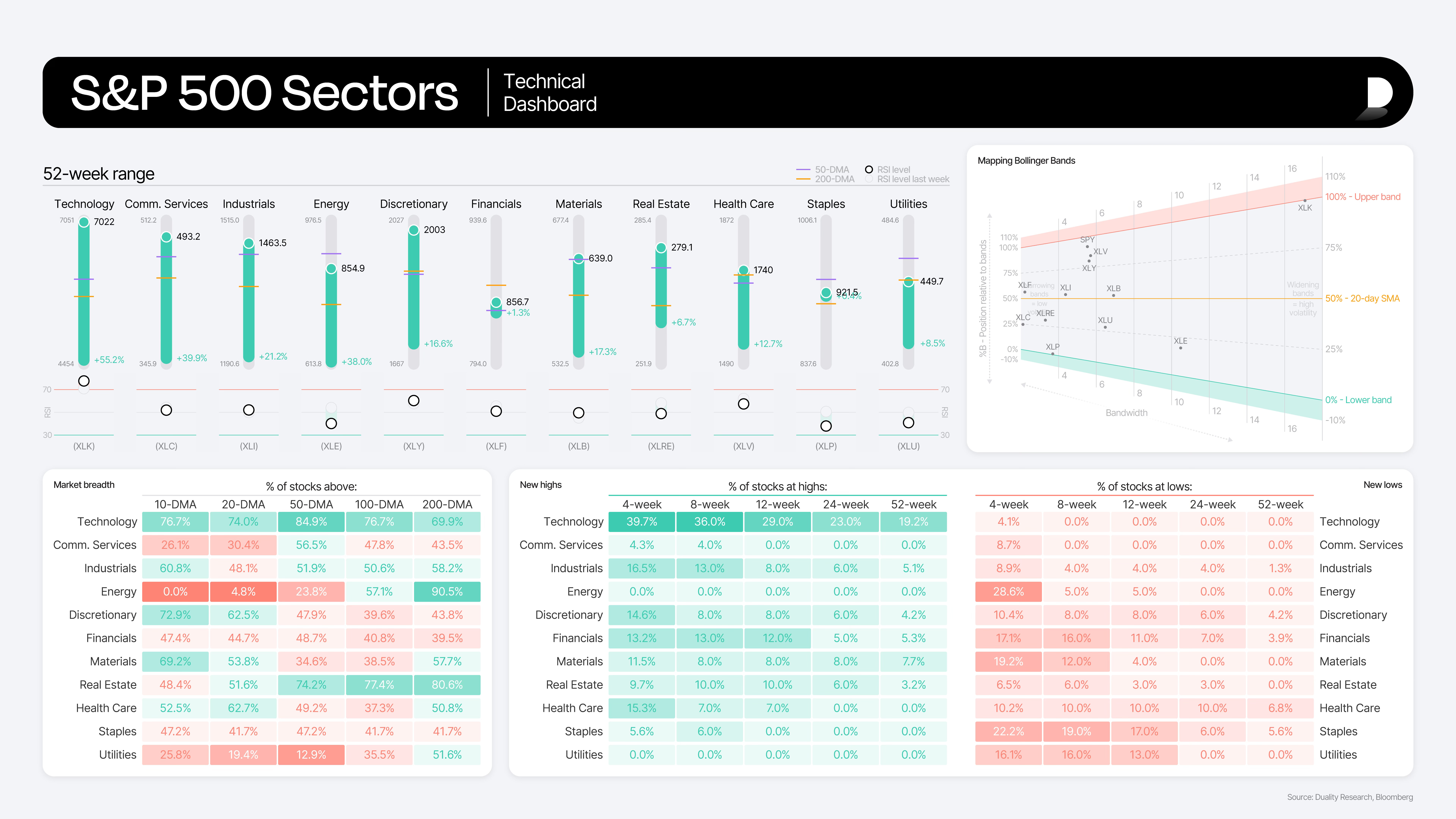

Semi’s are the market leader and are giving signals that the market is at an incredibly fragile point.

#1 Print in SOXX hit last week

A few interesting earnings reports this week including CRWD, PANW, MDT, and LULU.

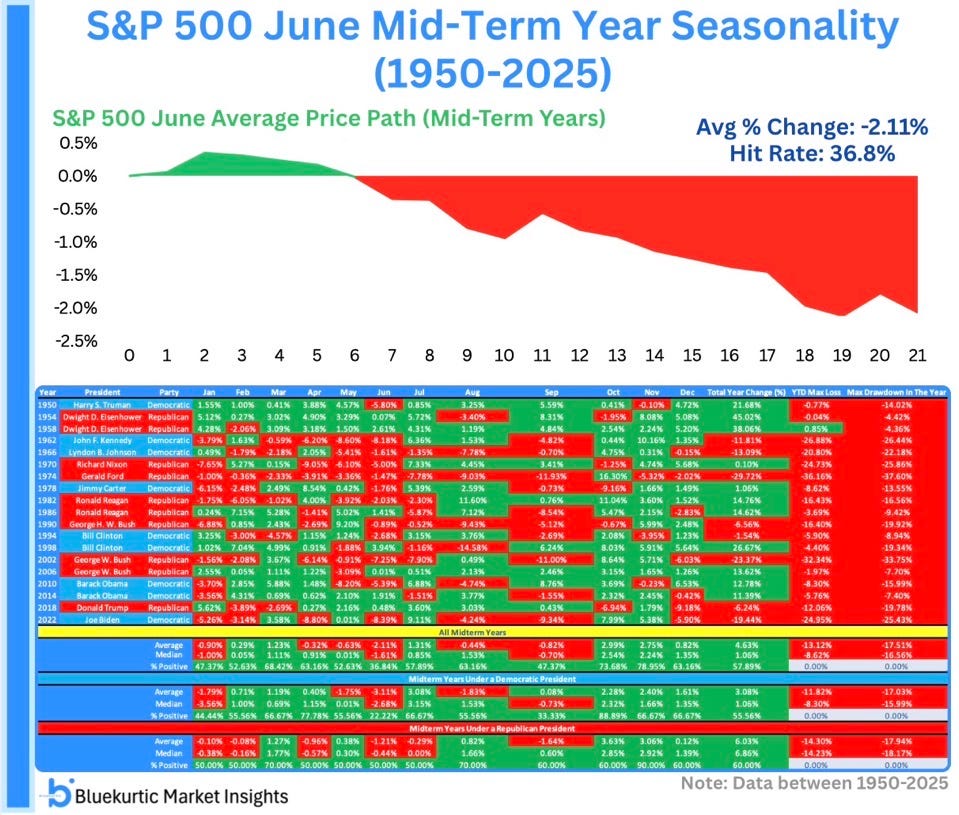

June Seasonality — Mid-Term Years (1950–2025)

June has been one of the weakest months on the midterm-year calendar. Across all midterm Junes since 1950, the S&P 500 has averaged -2.11%, finishing higher just 36.8% of the time — a poor risk/reward setup on its face.

But the path matters as much as the print. Stocks have historically held firm through the first week of the month, drifting modestly green before rolling over. The damage concentrates in the back half: the average price path erodes steadily from mid-month onward and tends to close near its lows. Early-June strength has been a trap more often than a trend.

The partisan split adds a wrinkle worth flagging.

Under Democratic presidents, midterm Junes have been brutal — averaging -3.11% with positive returns just 22% of the time.

Under Republican presidents, the month is far more benign: roughly -1.21% on average and a coin-flip 50% hit rate.

With 2026 sitting in the Republican-president bucket, the cleaner analog argues for chop and a mild downward drift rather than the deeper seasonal air pocket the headline number implies

Sentiment and Positioning

Bank of America’s Bull & Bear Indicator has quickly bounced back to extreme bull readings and consumer confidence for higher stock prices hit the 2nd highest reading ever. This confirms some euphoria here.

Shiller PE Ratio continues to climb, only being topped by the Dot Com Bubble.

Yes we have low forward PE readings for certain leaders but these are cycles and the market will begin to price in peak earnings at some point for some of these players that are leading the market currently.

Market breadth remains healthy despite Friday’s softening.

Percentages of stocks above the 5/20/50/200-day all dipped Friday but held above the 50% line, and the 5-day rolling over faster than the 20-day reads as a likely selldown-then-bounce rather than a top.

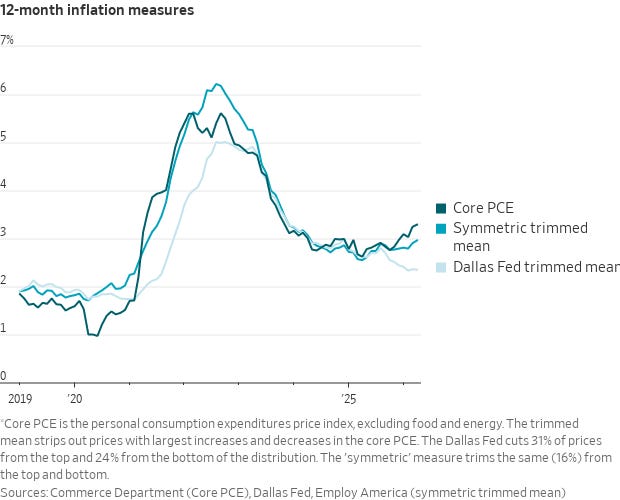

Incoming chair Kevin Walsh was chosen because he wants to cut, leaning on trimmed-mean PCE (2.4%) over core (3.2%) and headline (3.5%) and an “AI is deflationary” argument, and is expected to push back against the bond market’s hike pricing.

The market is overstating how hawkish Kevin Warsh would be as a potential new Fed chair.

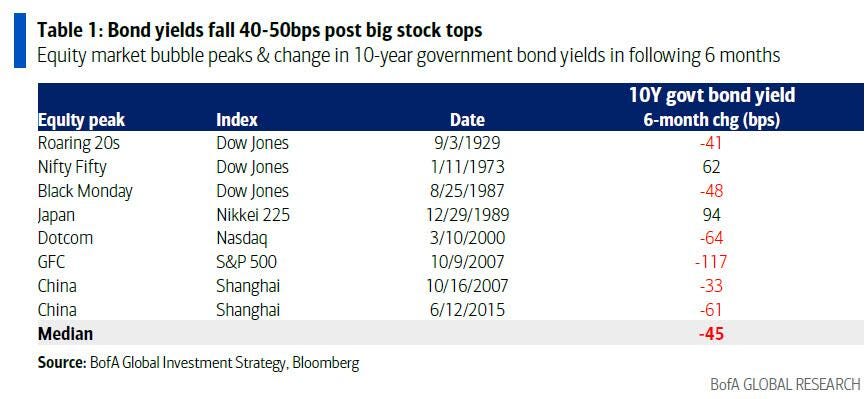

His first FOMC as chair comes June 17th and think sets up some interesting trades I’ll share later. But here’s a clue, with oil price action and Warsh following the lower inflation metrics, the argument for yields topping is already strong, add in the possibility of a bubble popping sometime over the next few years, there is a very strong setup based on previous market cycles. 👇

There are pockets of the market that complicate the argument for a pending top.

Small caps and software remain overlooked, under-owned, and cheaply valued relative to the megacap complex driving the index. That divergence matters. It tells you this is not a uniformly overheated market — it’s a top-heavy one, where the concentration risk is real and the opportunities for differentiated positioning still exist if you’re willing to look away from the headline index.

I’ll release the exact names and sectors I’m positioning into for paid subscribers on Tuesday.

If you have been on the fence, the next phase of this market I think will continue to be challenging and we are only warming up for the insights shared on how to navigate it. Consider joining for all the latest updates each week. Cheers.

I emphasize the opportunity in under-owned, cheaply valued sectors like small caps and software, while cautioning against overexposure to the overheated megacap complex. This is a differentiated perspective and actionable advice for readers navigating the current market environment.