The Old Rules Still Work — Because Markets Don't Change, People Do

A field guide to the maxims that have survived a century of crashes, and the men who lived (or died) by them.

Someone posted a market rule this week that could fit on a napkin and thought it would be a good write up:

That’s it. No chart. No 47-tweet thread with a Linktree at the end. Just one line — and honestly? It’s right. Not because it’s some genius insight, but because it describes human behavior that hasn’t changed since the Dutch were out here trading tulip futures in 1637.

Here’s what I want you to understand: these aren’t really rules about markets. They’re rules about people. Exchange hours, settlement systems, order flow — all of that evolves. But the thing that makes a parabola go vertical and then crater? Fear. Greed. The gut-punch of FOMO. The even worse feeling of being the last one holding the bag. That part of our wiring hasn’t changed, and it’s not going to.

I’ve lived and traded through enough cycles now to tell you — the rules that survive aren’t the flashy ones. They’re the ones with a mechanism behind them. A rule you can’t explain is a rule you’ll abandon the second the pressure is on. A rule you actually understand is one you’ll hold when your hands are shaking.

Let’s go through them.

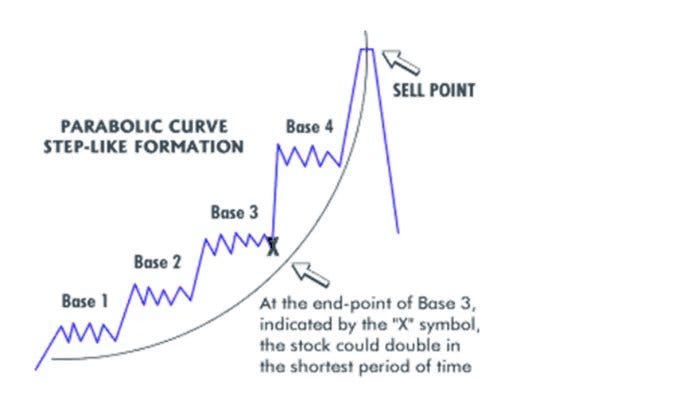

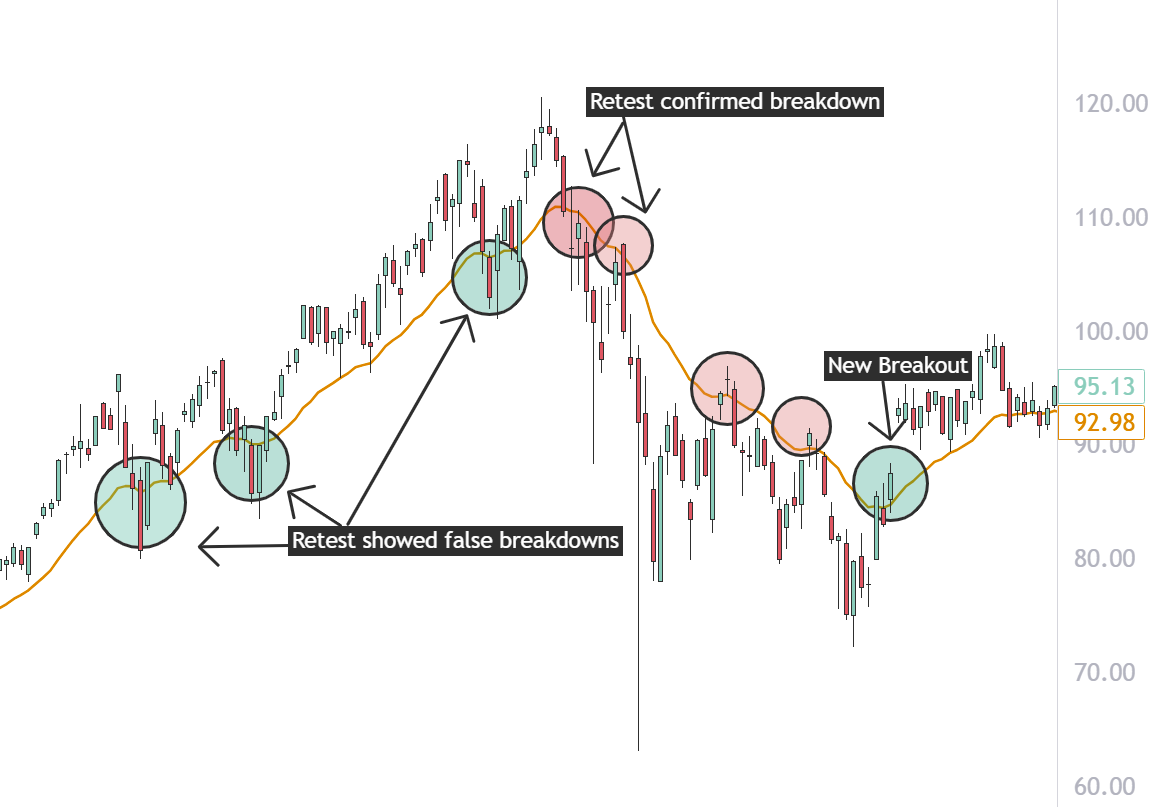

1. Sell Parabolic Moves

Why it works: When a chart goes parabolic, what you’re really looking at is demand being pulled forward all at once — FOMO longs piling in, trapped shorts panic-covering, dealers hedging gamma exposure. All of them are structurally forced to buy. And forced buyers have one big problem: they run out. When the last one’s finally in, there’s no one left to sell to. Price doesn’t drift down — it falls through a trapdoor, because that bid was never real demand. It was mechanics. For longs you're trailing: a close back below the 8- or 9-day EMA typically ends a parabolic ride. I like to scale out into vertical strength rather than waiting for the top: sell thirds — first into the climax volume bar, more on the first lower high. If timed properly, there is great potential profit fading the lower high as well.

Jesse Livermore is the patron saint of this rule. He shorted the panic of 1907 and then bet against the 1929 crash so hard he reportedly walked away with around $100 million — something like $1.8 billion today — in a single autumn. His edge wasn’t a signal. It was patience. He said the money was made not in the buying or the selling, but in the sitting.

The lesson underneath the lesson though? Livermore knew every rule in this post and still died broke in 1940 — having broken all of them. Knowing the rule and executing it are two completely different things. The market doesn’t grade you on what you know.

2. Be Greedy When Others Are Fearful

Why it works: At a real bottom, the marginal seller isn’t some rational actor — it’s somebody who has to sell. Margin calls. Redemptions. Pure psychological capitulation. They’ll hit any bid. That’s why the best prices in history printed when the news was the absolute worst. You’re not buying a great company at the bottom. You’re buying someone else’s panic at a discount.

The example shows each time since 1998 the VIX (Some call it the true fear index) was greater than 45 signaling true fear in the market. The forward returns average positive a month later in each occasion including the Dot Com Bust, Financial Crisis of 2008, and even Covid.

Everyone knows Buffett’s version: “Be fearful when others are greedy, and greedy when others are fearful.” But I always liked the original. Baron Rothschild allegedly said the time to buy is “when there’s blood in the streets” — a line he earned by buying into the panic after Waterloo.

The cleanest execution of this principle I’ve ever studied belongs to John Templeton. In 1939 — Hitler is rolling through Poland, the world is on fire — a 26-year-old Templeton borrowed money and bought 100 shares of every stock on the NYSE under a dollar. 104 companies. Several already in bankruptcy. Maximum pessimism, maximum mispricing, maximum mechanical selling. He quadrupled his money. Seven words summed up his entire philosophy: “Buy at the point of maximum pessimism.”

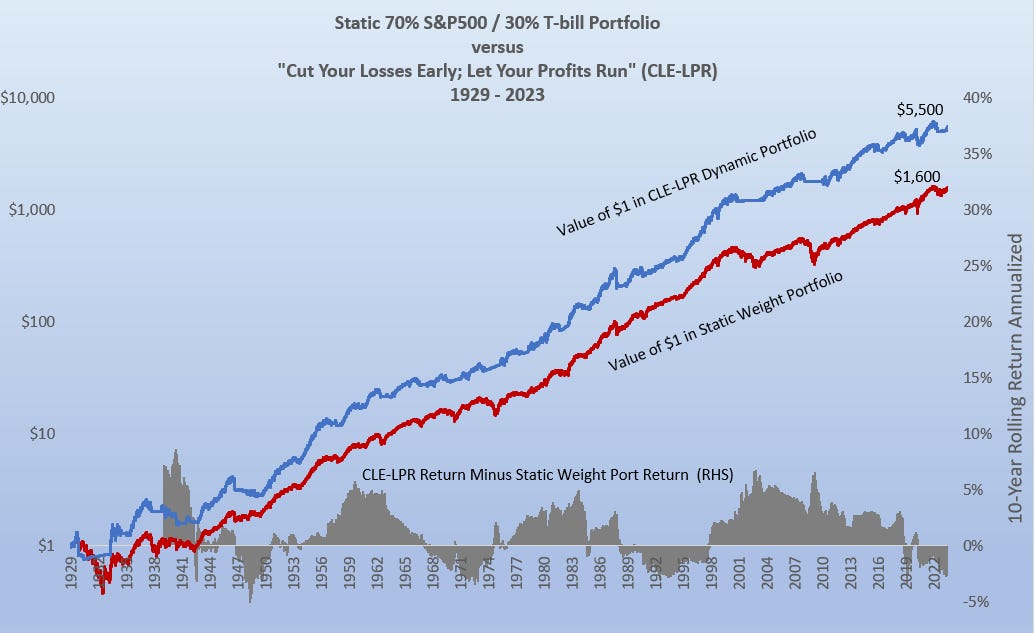

3. Cut Losers, Let Winners Run

Why it works: This is pure math fighting human psychology — and psychology wins almost every time, which is why almost nobody actually does it. A 50% loss requires a 100% gain just to break even. The math is brutal. But the pain of locking in a loss makes us hold losers hoping to “get back to even,” and the fear of giving back a gain makes us sell winners early. We do the exact opposite of what the math demands.

The math shows the CLE-LPR Strategy works well over time, although I think of this strategy more with swing trading versus investments where conviction is important.

For winners: trail with a rising MA (20-day for aggressive, 50-day for patient) and only exit on a clean break — let the trend, not nerves, make the call.

Paul Tudor Jones built his entire approach around the inverse instinct. He predicted the October 1987 crash and reportedly tripled his fund on Black Monday while the Dow dropped 22% in a single session. His mindset was unsentimental: losers average losers. He cut fast, ran winners, and treated capital preservation like the whole job — “Don’t focus on making money; focus on protecting what you have.”

4. The Market Can Stay Irrational Longer Than You Can Stay Solvent

Why it works: Being right about direction and wrong about timing is, financially, the same as being wrong. If your thesis is correct but your margin runs out first, you lost. This is what kills bears specifically. Bearish theses are usually eventually right — valuations do mean-revert, bubbles do pop — but “eventually” can come 18 months and one blown-up account too late.

Wait for confirmation before fading — don't short a parabola while it's still going vertical. Use a trigger: a lower high, a break of the 20-day EMA, or a failed retest. Let the trend break before you bet against it.

Here is an example of how the Dot Com Bubble could have been played properly using this strategy

The line is attributed to Keynes, and even if that attribution is shaky, the truth isn’t. Keynes himself nearly blew up his own account in the 1920s being early and over-leveraged on currency bets. He survived, adapted, and became a great investor. But it almost ended before it started.

What All of This Is Actually About

Look at what every single one of these rules has in common. It’s not earnings. It’s not Fed language. It’s not some indicator crossover. It’s forced participants — buyers who have to buy and sellers who have to sell — and your job is to be on the other side of their desperation. The parabola is forced buyers exhausting themselves. The bottom is forced sellers capitulating. The crash is forced longs getting liquidated. Find the participant with no choice. Take the other side.

And then there’s the darker thread running through all of this: nearly every name in this post knew these rules cold and still got hurt the moment emotion overrode discipline. Livermore died broke. Druckenmiller torched $3 billion. Keynes nearly washed out. The rules themselves are simple enough to fit in a tweet and end with “Have a nice day.”

Following them when every nerve in your body is screaming the other way — that’s the whole game.

Markets don’t change. People don’t change. Which is exactly why a rule written for tulip traders still applies to whatever chart you’re watching right now.

Sell parabolic moves. Have a nice day.

Nothing in here is investment advice. This is market history and behavioral pattern recognition — the kind that’s survived a hundred years because the thing it describes never does.

Is AI the End of ServiceNow — or Its Next Leg Higher?

There are very few companies in the software world that have earned the right to be called compounding machines. ServiceNow is one of them. From a niche IT service management platform to the de facto operating system for enterprise workflows, $NOW has executed its expansion playbook with remarkable consistency — growing gross profit at a 28% CAGR and fr…

The balance between historical patterns and evolving markets is key—rules stay, but their execution must adapt. For example, while 'sell parabolic moves' remains valid, today's algorithmic trading adds new layers to how those mechanics unfold.