The Week Ahead 2/1/2026

Shadows in the Uptrend

Market tone continues to shift as investors confront the early signs of a sentiment reversal. Following an extended stretch of one-sided positioning and stretched valuations, risk appetite appears increasingly fragile heading into the heart of Q1 earnings season. Over the weekend, a mix of stress signals emerged — regional bank failures, crypto liquidations, geopolitical flare-ups, and renewed uncertainty in the AI and semiconductor space — all adding pressure to an already crowded trade. Technology and large-cap names, previously market leaders, now look vulnerable to mean reversion as positioning and momentum unwind.

Precious metals reflected this shift as well, with silver finally rolling over after several weeks of speculative enthusiasm. The metal’s breakdown aligns with our earlier expectations for a broad recalibration of risk assets. For equities, we continue to monitor SPY’s defined ranges closely; underlying support levels form the line between a shallow pullback and a more meaningful risk-off phase. Overall, conditions suggest an environment where rallies are increasingly sold into, and a rotation into more defensive names may be signaling a risk off environment isn’t far away.

Via - Almanac Trader

Index’s

SPY - S&P 500

Historically, a positive January has skewed the odds toward a strong year, with the S&P 500 posting an average February–December gain in the low‑double digits and finishing higher roughly 80–90% of the time. Our attached chart reinforces that pattern: when January is green, the “rest of year” tape is usually constructive, but there is a non‑trivial minority of cases where macro shocks still produce meaningful drawdowns along the way. In our view, this backdrop argues against anchoring on a prolonged bear market as the base case for 2026 and instead supports a regime where corrections are sharp but attract buyers relatively quickly, particularly around well‑defined support zones. Within that framework, we continue to treat SPY’s key support and resistance levels as the primary risk‑management map for the quarter, expecting rallies into prior highs to meet supply while deeper pullbacks are met with systematic and discretionary re‑risking rather than wholesale de‑leveraging

While the 1st half of February is generally a positive window, when compared to other months the tailwind doesn’t seem that strong. If anything, this could give an opportunity to position for more risk ahead. Historically, the 1st day of February is positive, so wouldn’t be surprised to see this weekend dip bought.

Systematic trend‑following funds remain heavily long S&P 500 futures after the persistent rally, and their models are clustered around well‑defined “flip” and unwind thresholds not far below current prices. Once those levels are breached, CTAs shift from marginal buyers to incremental sellers, with recent estimates suggesting tens of billions in potential equity futures supply over a short window in a full de‑risking scenario.

QQQ - Nasdaq

For QQQ, the volatility picture is increasingly asymmetric. The weekly chart shows Bollinger Band Width compressed back toward historical lows, a setup that has historically preceded sharp directional moves as ranges resolve and volatility expands. In options terms, the tape looks more like a “coiled spring” than a trend in motion, which argues that investors should be thinking about magnitude of the next move at least as much as direction

This analysis from MarketCharts also stood out to me as something to watchout for in the coming weeks. The setup looks similar to previous price action before corrections.

Sectors

XLE - Energy

The percentage of S&P 500 energy constituents trading above their 50‑day moving average has pushed up into the mid‑90s, a zone that has historically marked short‑term overbought conditions and preceded periods of mean reversion rather than continued linear upside. However, geopolitical catalyst are often > than technicals

Overall my base thesis is for Energy to continue a strong performance in 2026.

via - All Star Charts

Software - IGV

Software is increasingly looking like a late‑stage laggard trade rather than a momentum leadership group, but the risk‑reward is starting to skew more two‑sided.

Software components are trading well below their 52‑week highs, with average drawdowns sitting in the high‑30s percent range and the sector recently slipping into a defined bear‑market drawdown from its peak. That degree of de‑rating typically precedes at least tactical relief rallies as sellers exhaust and incremental bad news becomes less effective at driving fresh lows, which keeps our base case tilted toward a bounce as we move through upcoming catalysts

Crypto

Bitcoin with continued weakness over the weekend, watch for a hold and retest of breakdown. Daily RSI showing oversold read but a continued flush could test 72k level before reclaim. Expect to bottom in October based off previous cycles but there will be chop along the way.

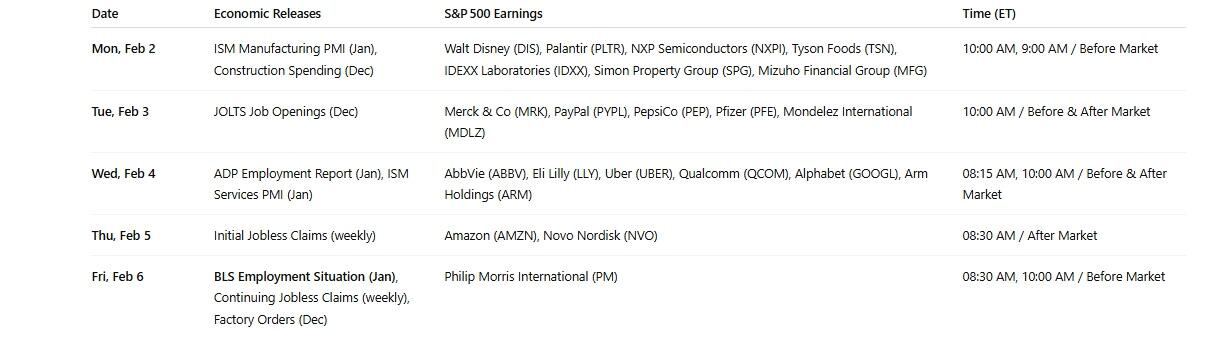

Catalyst This Week

This week’s macro and micro calendar is dense enough to challenge the prevailing soft‑landing narrative, with key data on activity, employment, and services inflation landing alongside high‑profile earnings and a newly uncertain Fed leadership outlook. With positioning stretched and volatility compressed, any material deviation from expectations—on growth, labor, or the path of policy under Fed‑chair‑designate Kevin Warsh—has the potential to spark outsized moves across rates and risk assets

Final Thoughts

Risk is quietly but steadily stacking up, and I’m treating this as a phase to play defense first and offense second. Sentiment is back near extremes, insider selling is picking up, and several of the signals that started flashing in December—most notably the VIX term structure—are rolling back into view and have historically aligned with corrective phases rather than fresh upside acceleration.

With expectations for both earnings and macro outcomes priced aggressively, the market feels increasingly vulnerable to any disappointment or left‑field headline, especially as we continue to get a daily drip of new geopolitical, policy, and idiosyncratic risks. In that environment, I believe a more defensive stance is warranted.

For paid subscribers, I’ll be releasing my specific trade ideas and positioning maps for the week ahead, including where I’m looking to fade rips, which sectors I’m targeting, and the tactical hedges I’m considering as the market begins to price in a wider range of outcomes.

Recent Feedback

Hope you all enjoyed the content, a restack or review is always welcome. Cheers!