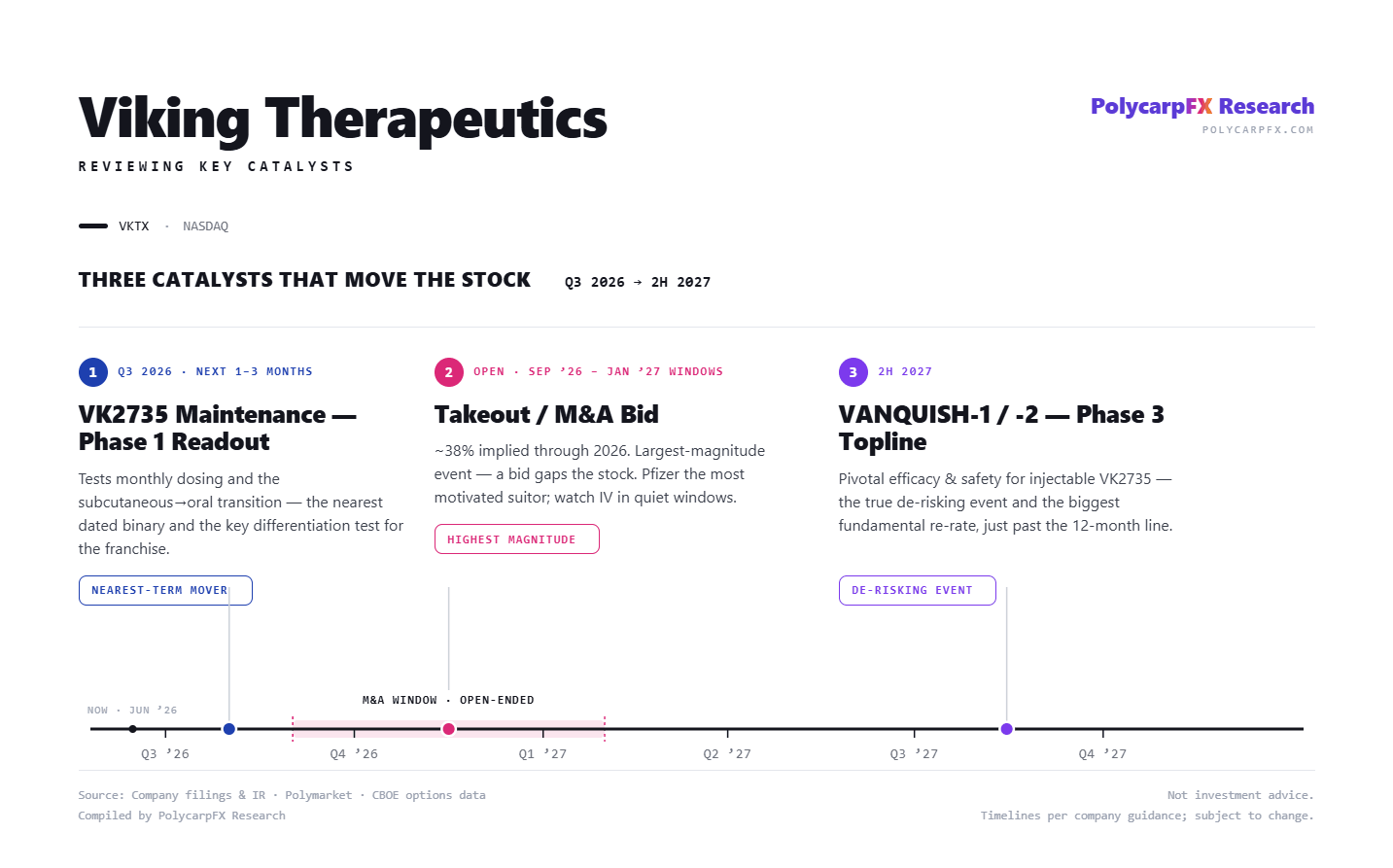

Will Viking Get Bought in 2026? Key Catalyst Ahead

VK2735 is arguably the most advanced obesity asset still sitting outside Big Pharma’s walls

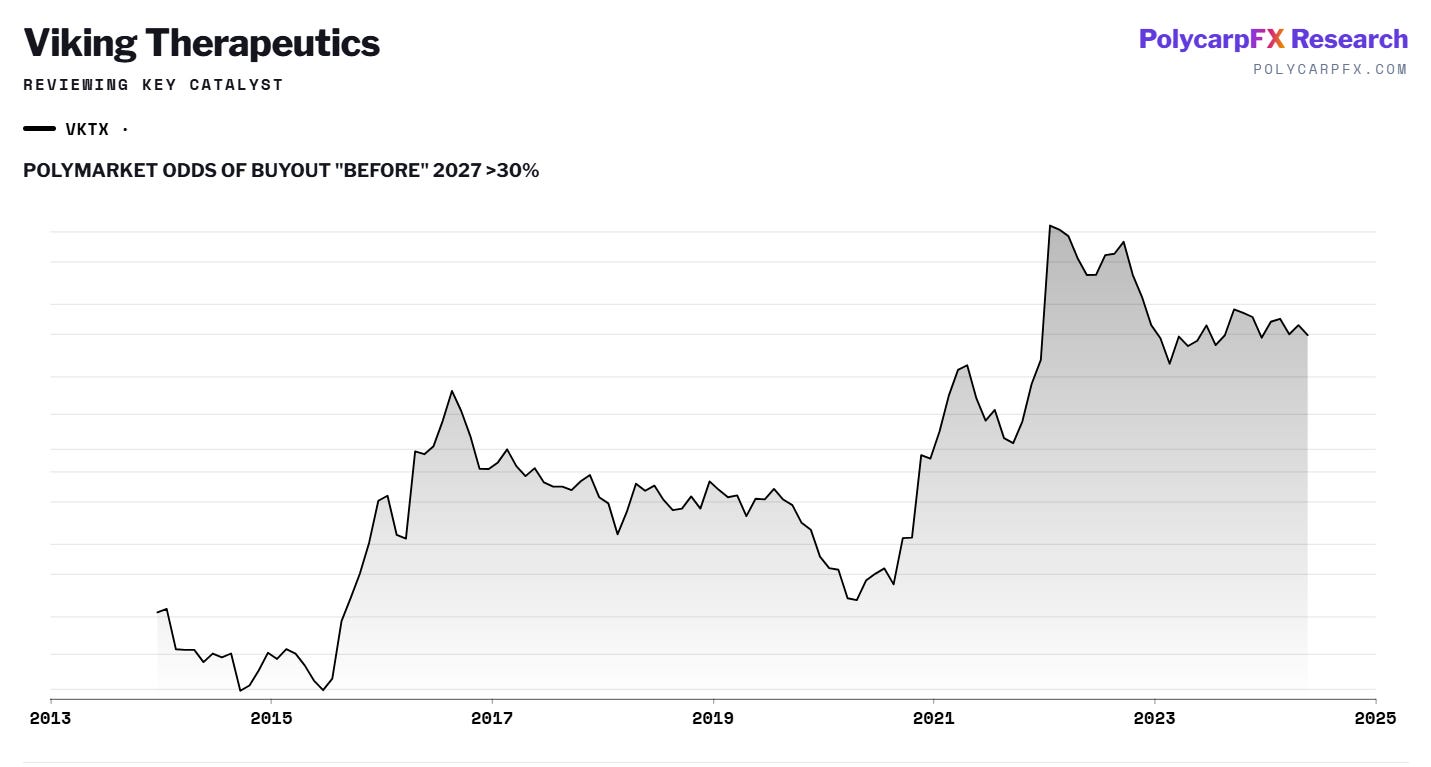

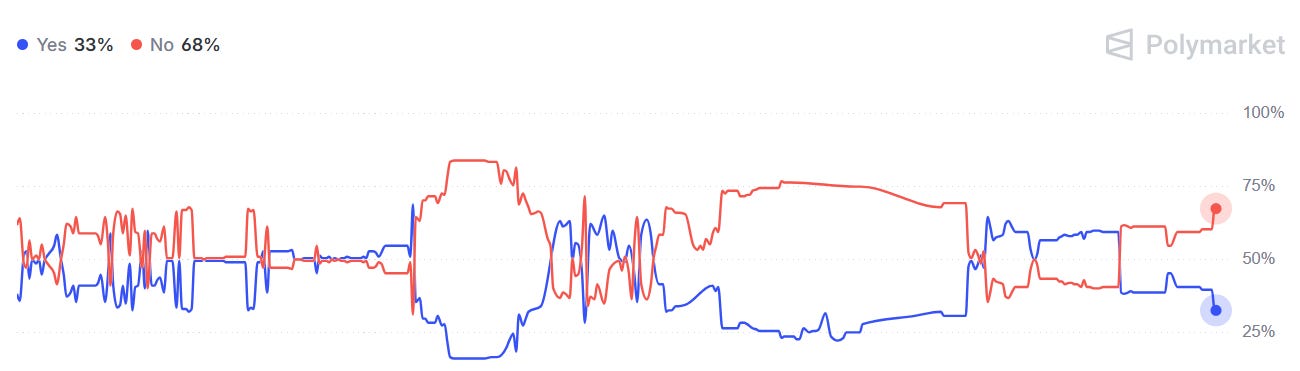

A quick note on takeout odds for VKTX — and why the timing question matters more than the target question.

That Viking Therapeutics is a takeout candidate isn’t controversial. VK2735 is arguably the most advanced obesity asset still sitting outside Big Pharma’s walls — a dual GLP-1/GIP agonist in both subcutaneous and oral form, with the subcutaneous program fully enrolled in two Phase 3 trials. At a market cap near $3.6B and a cash balance around $600M, it’s small enough to swallow and dangerous enough that the incumbents can’t ignore it. The interesting question isn’t whether a deal is plausible. It’s whether one lands in 2026 specifically — and there the picture is more nuanced than the headlines suggest.

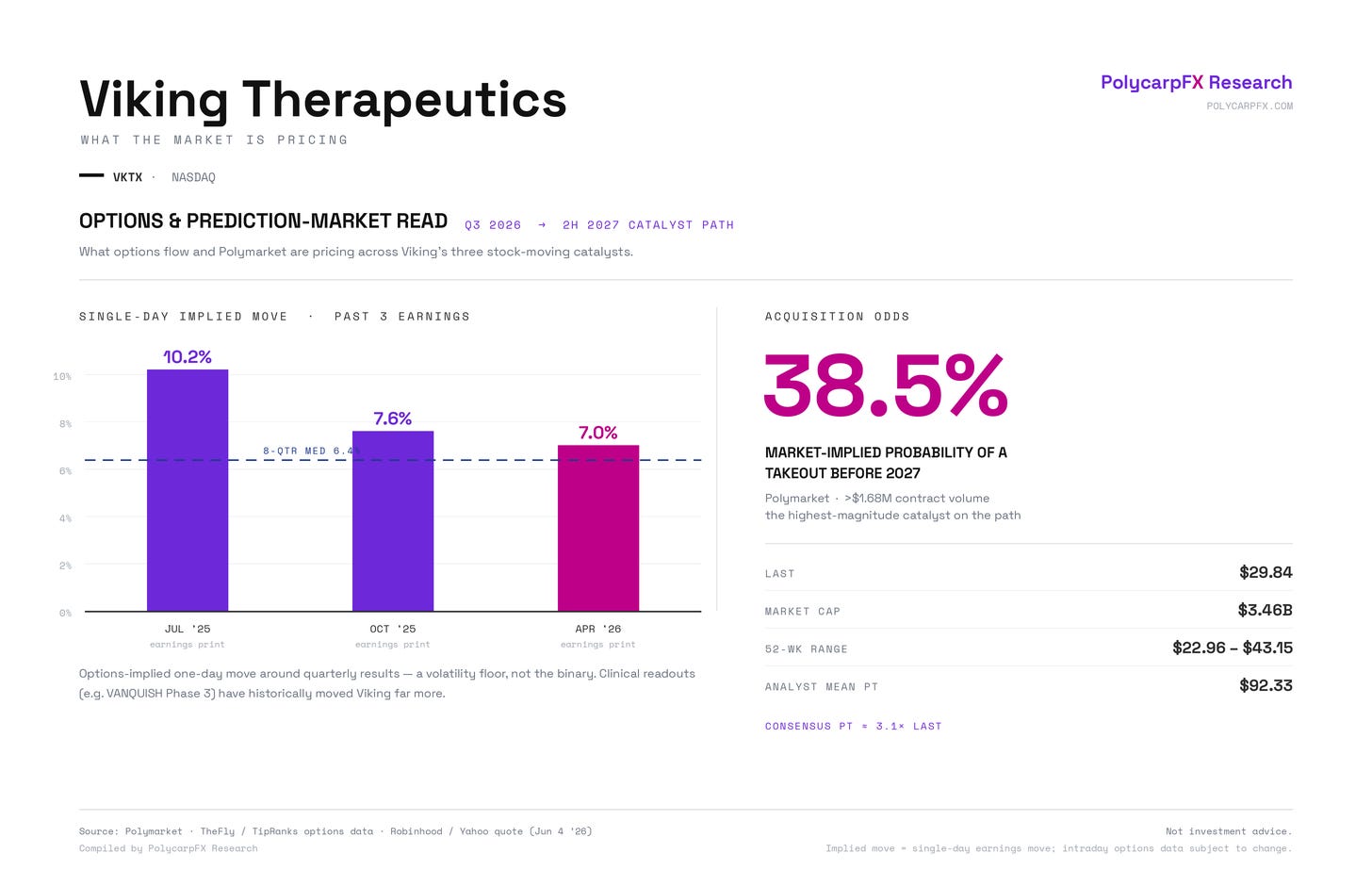

The market is pricing a real, but not dominant, probability. Prediction markets put the odds of an acquisition before 2027 around 33%, with enough volume behind the contract to take it semi-seriously. The options chain rhymes with that: open interest is heavily call-skewed (roughly 4:1 calls over puts), with meaningful long-dated call positioning out at the January 2027 expiry — i.e., money parked past the pivotal data window. That’s consistent with traders underwriting an upside gap, whether from clean trial data or a bid. The caveat for anyone reading too much into implied vol: VKTX carries structurally rich vol anyway because of its binary clinical calendar, so you can’t cleanly separate “takeout premium” from “data premium.” Bullish positioning, yes. Confirmed deal signal, no.

The buyer bench is real but uneven:

Pfizer — the most motivated name. It has been the most active obesity acquirer, is building out the Metsera platform, and has openly framed 2026 as a catalyst-rich, business-development-heavy year. A Phase 3-ready dual agonist slots directly into that strategy.

Novo Nordisk — the defensive case. With share under pressure and soft guidance, a bid to protect the franchise is plausible, if not its preferred move.

Eli Lilly — less urgent than it was. With its own once-daily oral pill now approved, the strategic need to buy an oral asset has softened, and antitrust optics around the category leader complicate the fit.

Merck / Amgen — longer shots that round out the list.

Here’s the tension that actually governs 2026. The pivotal VANQUISH readouts — the data that truly de-risks the asset — don’t arrive until the second half of 2027. So a disciplined acquirer has a clean reason to wait. The counter-argument, and the one bulls lean on, is that you don’t wait for the data if waiting means bidding against three rivals at a much higher price. Pre-empting a post-data auction is exactly how early biotech bids happen. Cutting the other way: Viking just brought on a chief commercial officer to prep a launch — a posture that reads as “willing to go it alone,” which only raises the number any suitor has to put on the table.

Bottom line: treat 2026 takeout as elevated, market-priced optionality — a ~38% tail against a hot obesity-M&A tape — not as a base case. The asset is desirable, the buyers are shopping, and the positioning leans bullish. But the cleanest value-inflection event is a 2027 story, and nothing in the current evidence rises above strategic logic and speculation. Own the optionality if you want it; don’t underwrite the deal as a foregone conclusion.