The Gauntlet: CPI, Oracle, and the Largest IPO Ever

The Week Ahead - June 8th, 2026

A week that printed fresh record highs midweek reversed hard as chips cracked, Seoul tripped a circuit breaker, and Treasuries sold off. With payrolls running hot and inflation drifting away from target, does next week's CPI force the higher-for-longer trade back to center stage — right as the largest IPO in history hits the tape?

The Week That Was

It started euphoric and ended defensive. Equities pushed to new records into midweek before a chip-led reversal swept the major averages lower and snapped volatility out of its springtime calm. I wrote about this setup on Tuesday for those who missed it.

The Engine & The Risk

The S&P 500 is quietly doing something remarkable. We’re now on the 9th consecutive up day — the longest streak since May 2025 — and sitting on the cusp of a 10th consecutive up week, a run not seen since 1985. Let that sink in for a moment. 1985.

May payrolls came in at 172K against an ~80K consensus — more than double expectations, with several firms flagging World Cup-related hiring (the tournament opens June 11). A blowout jobs number in a higher-for-longer regime is a tightening, not a tailwind, and it reignited the rate-cut-versus-rate-hike debate hours before the weekend. My lean is that this is short lived from a labor perspective due to world cup seasonality and much of the damage caused in the market was more driven by stretched technicals.

Semis & AI capex

The spark was Broadcom’s after-hours print: management held its full-year AI outlook roughly flat and guided next quarter a touch below the Street’s elevated bar. After a torrid run, that was enough to flip sentiment — chips led a broad tech selloff into Friday, the Philadelphia Semiconductor Index’s worst session in over a year, with memory and equipment names hit hardest. The debate has shifted from whether AI capex is growing to whether the estimates got too high.

Korea & memory

The same trade unwound harder overseas. The KOSPI tripped a circuit breaker after a blistering multi-month run, led lower by SK Hynix and Samsung — the two names that dominate the index’s market cap and the bulk of its year-to-date gains. Record margin balances and a wave of leveraged single-stock ETFs amplified the move. With the Bank of Korea widely expected to hike in July, the memory cycle remains the cleanest global read on the AI-hardware trade.

Rates & the dollar

The jobs surprise sent Treasuries lower across the curve, pushing the long end back above the 5% line and the dollar to its firmest level since the spring. “Good news is bad news” is back: every strong data point now reads as a reason for the Fed to stay put — or worse.

Flow

Watch the leverage at the edges. MicroStrategy disclosed its first bitcoin sale in roughly 41 months — a symbolic crack in the “never sell” posture — and bitcoin drifted lower on the week as the reflexivity debate around corporate crypto treasuries resurfaced.

The Week Ahead

A loaded calendar, and all of it lands inside the pre-FOMC blackout — the June 16–17 meeting is Kevin Warsh’s first as chair, complete with fresh dots. No Fed speakers to lean on; the data and the deals carry the tape.

Data (8:30 a.m. ET)

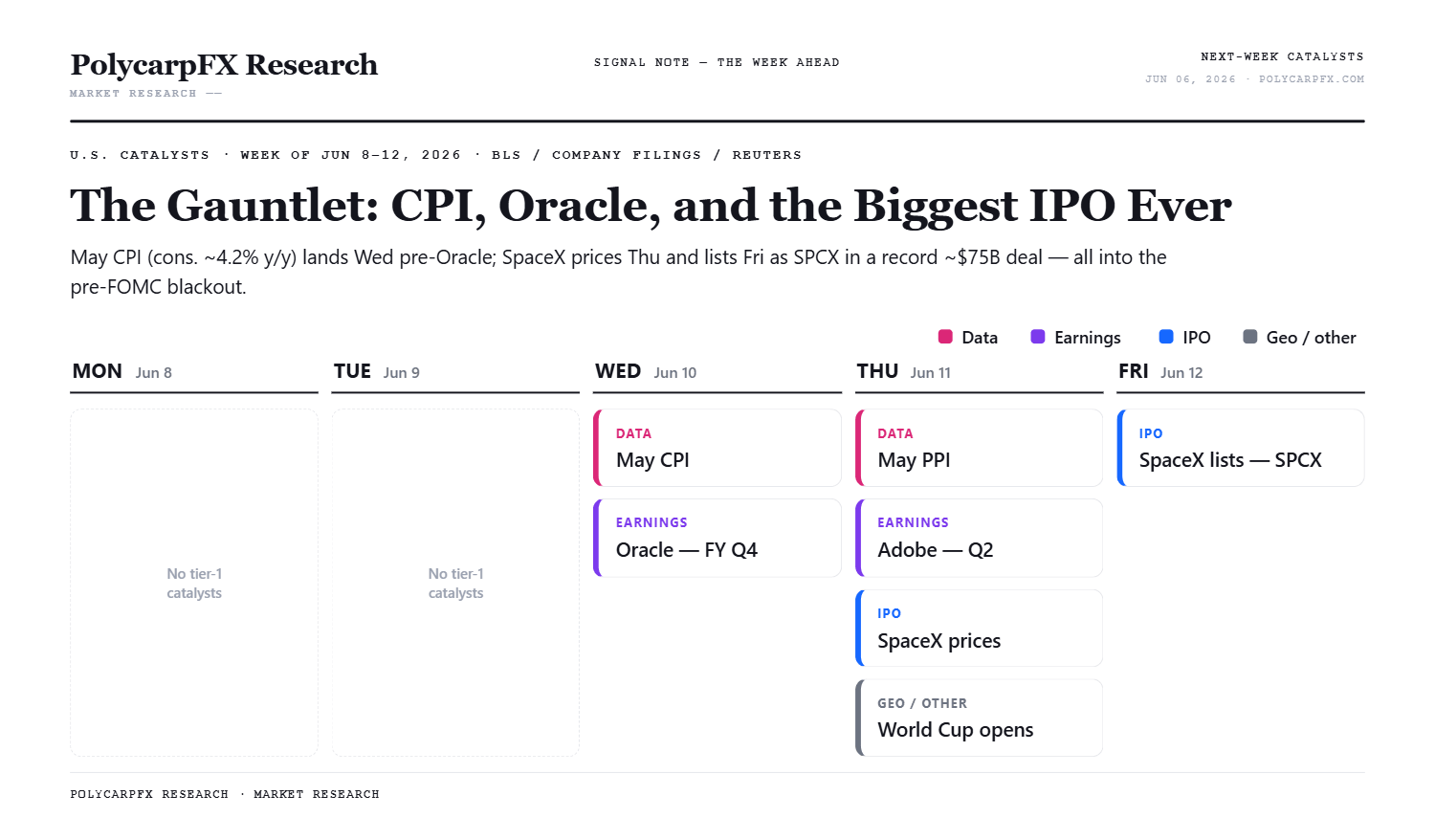

Wed, Jun 10 — CPI (May). The marquee. April headline ran at a three-year high; nowcasts point to a further pickup near 4.2% y/y — roughly double the Fed’s 2% target. Core and the energy pass-through from the Hormuz disruption are the whole game.

Thu, Jun 11 — PPI (May) + weekly jobless claims.

Tue, Jun 9 — International trade (April), wholesale trade. Retail sales and PCE fall the following week.

Central banks

FOMC blackout into the June 16–17 decision; futures lean toward a hold, but the market has been adding to the odds of a hike later in the year.

Bank of Korea — no meeting this week; next decision mid-July, with a hike widely expected.

Earnings

Wed, Jun 10 (after close) — Oracle (ORCL), Q4 FY26. The cleanest AI-capex read of the week — cloud bookings and OCI backlog land the same day as CPI. Oracle tends to move sharply on results.

IPOs / lock-ups

Thu, Jun 11 — SpaceX (SPCX) prices; Fri, Jun 12 — lists on Nasdaq.

A record-size offering (~$75B raise, ~$1.75T valuation, ~30% retail allocation) — the largest IPO in history — debuting into a tape that just saw its worst chip session in over a year. A live gauge of risk appetite.

Geopolitical

Strait of Hormuz / Iran — the namesake thread stays hot. The strait has been effectively shut since late February and the ceasefire remains fragile (fresh missile exchanges, a rejected truce track). Oil is elevated and headline-driven — the swing factor under the CPI path.

World Cup opens in the U.S. (Thu, Jun 11) — a services/demand tailwind already visible in payrolls.

Seasonality

2026 is a U.S. midterm election year, and that cycle carries one of the more durable seasonal patterns on the board. Historically the S&P 500 drags in the 12 months into midterms — averaging well below its long-run norm — then posts above-average gains in the 12 months after.

Trading Wisdom of the Week

Livermore’s line is the antidote to a week like this. After a sharp reversal the temptation is to do something — chase the bounce, flip short, average the dip — but the traders who compound aren’t the busiest; they’re the ones who can sit on a position (or in cash) without itching to act. With CPI, Oracle, and the largest IPO in history all landing within a few days, the edge isn’t clever pre-positioning — it’s the patience to let the catalysts resolve and to size up only when the setup is obvious. In a tape driven by leverage and emotion, doing nothing is often the highest-conviction trade.

What to Watch

CPI - A hot print (at/above the ~4.2% consensus, firm core) pushes the higher-for-longer trade and raises the odds the Fed’s next move is a hike — pressure on long-duration growth and rate-sensitive names. A cool print is the relief valve: with chips and Korea freshly washed out, it could fund a sharp oversold bounce into the SpaceX listing.

Oracle, same night, is the AI tell. After Broadcom’s guide, the market wants confirmation the data-center buildout is still accelerating — or another reason to question the estimates.

Cross-asset markers. The 30-year holding (or losing) the 5% line and the direction of the dollar will frame risk appetite all week; the prior record highs now sit overhead as resistance, with the spring breakout zone the first support shelf below. Oil and any Hormuz headlines remain the wildcard for the inflation path.

What would shift the narrative. A soft May CPI that pulls the long end back under 5% and an upbeat Oracle could re-ignite the AI bid and squeeze a heavily de-risked tape; conversely, a hot CPI plus a cautious Oracle would hand the bears continuation. A genuine Hormuz reopening (oil easing) would cool the inflation impulse through the back door.

Hope you enjoyed the read, if you aren’t a paid subscriber, consider joining the team as I give out company deep dives, discord access to my own trading journal, overall market analysis, and take request for data and insights on your favorite companies, cheers!

The Engine & The Risk

The S&P 500 is quietly doing something remarkable. We’re now on the 9th consecutive up day — the longest streak since May 2025 — and sitting on the cusp of a 10th consecutive up week, a run not seen since 1985. Let that sink in for a moment. 1985.

Really, really good. Thank you!

The market's reaction to CPI and the SpaceX IPO tests emotional discipline—a disciplined approach based on rules can help avoid chasing rebounds or overreacting to news.